Noise and an overwhelming amount of data is the biggest challenge in managing money in 2019 (or anytime in the past decade). In the 1960s, 1970s, and even the 1980s, delivering alpha came down to having access to information others didn’t have – the process of obtaining data was a value-add. Today, we have the complete opposite problem. In 2019 we have too much information, and delivering alpha comes down to paring things back to their essence, stripping away unnecessary garbage.

In the world of investing, there are some things that just don’t work: among these, we include rigorous data analysis and macroeconomic analysis. This is a controversial conclusion in an industry that has decided otherwise. What do we think does work? Simple historical analogs combined with rock-solid risk management techniques.

In this letter we’ll focus on the few pieces of information that we have sniffed out and are focusing on, to the exclusion of the other screaming headlines, articles, tweets, and blog posts that come at us a hundred times an hour. Our overarching thoughts (in no order):

- The Fed has made an incredible U-turn from a mere six months ago. In fact, this appears to be the largest and most drastic shift in policy expectations that we can think of over the past few decades. Where Jerome Powell once appeared to be a hawk, he’s been uncovered as the ultimate paper tiger.

- President Trump has recently referred to Powell as a “stubborn child” who “blew it”. The highlight of his recent tweeting came when he stated that he “should have Draghi instead of our Fed person”. This is hysterical and we sympathize with the fact that many people have tuned out Trump’s tirades. We think that’s a mistake. Trump was elected by half of the country in a populist wave, a wave that will outlive his presidency. Recent Fed interest rate hikes over 2017 and 2018 appear to be a counter-trend wave in a secular “easy” monetary policy regime. This narrative is further strengthened by the fact that Neil Kashkari is subtly offering his services as a potential replacement for Powell by saying he would have cut 50 basis points in June. What?! A 50 basis points cut with the stock market at all-time highs and no recession in sight is the surest sign of the current zeitgeist and the best anecdote that we have for what monetary policy will look like for the next decade or two (hint: it’s the anti-Volcker).

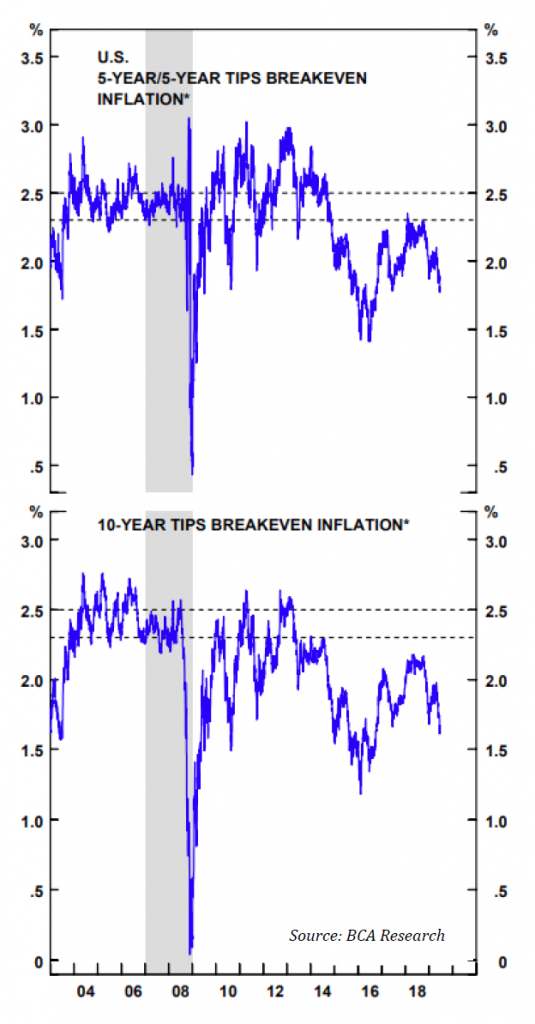

• As we have stated in the past, we live in times where the lenders of capital (bondholders) will be sacrificed over time in order to placate the restive masses. This is a secular trend that will last for decades to come, much as the deflationary trend that inflated asset values has lasted for the previous 35 years. Our candidate for “most important chart in macro” is to the right. The Fed will not allow these forward-looking inflation expectations to drop; expect the central bank to get its way and drive these breakevens higher over time.

• All fiat currencies will be a casualty of these trends, oscillating against each other but declining overall (on a secular horizon). On a shorter, cyclical horizon, we are very bearish on the dollar. Remember that it’s what is priced in that counts when inflection points occur, and the market has been pricing in a moderate Fed and an incredibly accommodative ECB and Bank of Japan. We believe that’s about to change in a big way.

AG Capital is a fundamental, long/short macro investment firm, trading across currencies, commodities, interest rates, and equity futures.

The firm follows a fundamentally-oriented, discretionary long/short macro investing. We look for opportunities where imbalance between supply, demand, and inventories (where applicable) may lead to a large price move. Position hold times vary from 1 month to years; no day-trading, no algorithmic trading. Fundamental analysis is used to determine directional exposure, both long and short. Technical analysis is used to determine trade timing: enter and exit positions where extreme asymmetry exists from a risk/reward standpoint.