Managed futures should not be synonymous with trend following but most of the major indices that track this hedge fund style have a high proportion of trend-followers. Because trend-followers are the biggest traders in the space, the indices will be driven by the market trends. No trends, no performance.

Managed futures will do better when there is a crisis, given there are usually big market distortions. Some call it crisis alpha, others refer to these events as market divergences, but when dislocations happen over not just days but weeks, managed futures will perform. If there is more sideways movement or choppy behavior with quick sharp reversals, performance will lag.

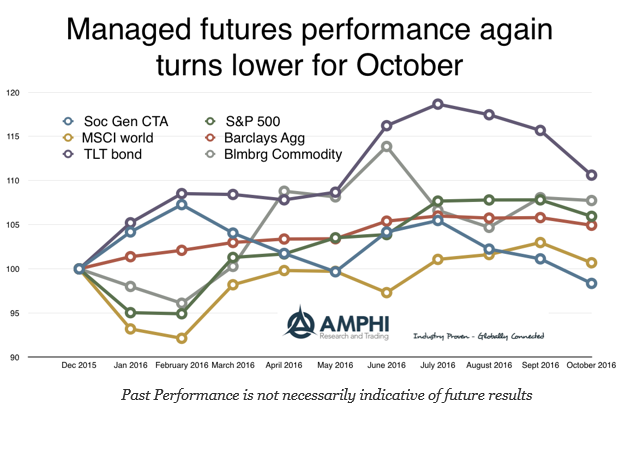

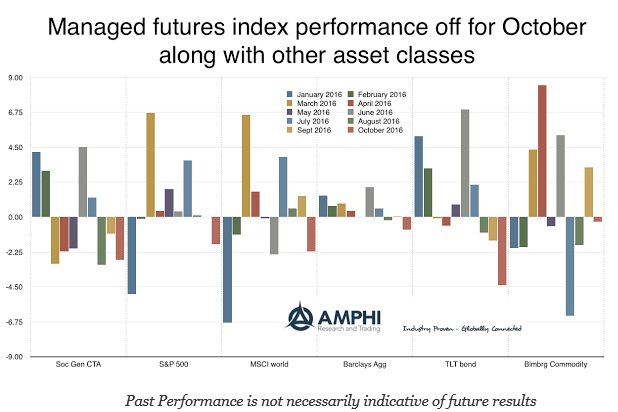

October was not kind to managed futures. The SocGen CTA index turned clearly negative for the year with regular declines since the strong showing in the first two months of the year. This month the decline was caused by a switch from risk-on to risk-off with growing fears of inflation and Fed action by the end of the year. The negative market returns were in both equities and fixed income. The traders in the index were not able to capture the price reversals. Growing trends in other markets were not enough to offset the larger moves in the two largest asset classes.

A close look at the CTA index versus bonds in 2016 show that the positive and negative moves often came during the same months; however, the positive bond moves were greater than the CTA gains and the loses were smaller. CTA’s were not able to capitalize on the greater dispersion in commodities or the big moves in equities. The heavy fixed income focus generally hurt managed futures this month.