It will be a tough investment world going forward for the simple reason the odds are against you. If you are a blackjack card counter in Vegas, you always know the odds, or the count. You know that on any draw, you can get lucky, but in some environments, the chance of success is just lower. Regardless of how smart you are, if the odds are not with you, your chances of getting good returns are lower. Your job as an investor is to know the odds and deal with the consequences.

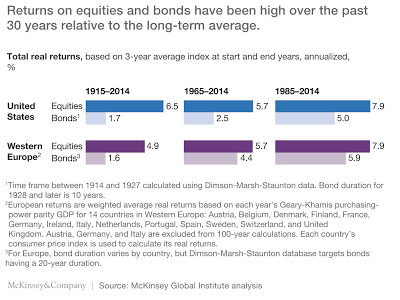

Well, bad odds are the current situation with returns for bonds and stocks going forward. It does not matter whether you are a good stock picker or know the bond market better than your peers. The long-term average returns are lower than what you have received over the last few years; consequently, it will be hard to make money if we just follow the averages. This is not a prediction for 2017 or a view that the longer a rally persists the more likelihood there will be a reversal. This view only states that if you look at long-term returns over the last three decades, the numbers were very good versus longer-term averages. This is the bleak view of McKinsey & Co.

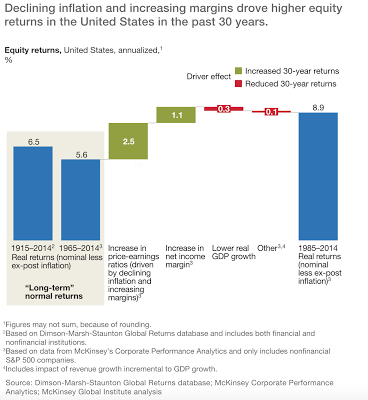

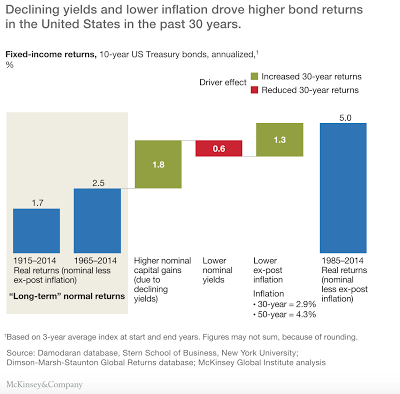

Granted their analysis is simplistic on the surface, but a decomposition of equity and bond returns over the last three decades tells us the environment going forward will not be able to generate the gains seen in the past. The main driver of both equity and bond returns has been lower inflation. The lower inflation allowed yields to decline substantially to our current low levels. Current yields cannot generate cash flow going forward and there are no drivers to push bond prices higher except bad growth. For equities, margins and lower inflation were able to provide strong tailwinds for equities. The inflation environment will not be favorable, valuations are not cheap, and margins may not be able to make up the difference for equities.

The bottom line is that assumptions for pension fund returns are just too high even if based on smoothed historical averages. Higher bond allocations will lead to lower yields and higher stock allocations may increase risk. The choice between the two major asset classes will not lead to a set of viable options.

The unrealized hope is that hedge funds will offer a third way to higher returns. Of course, this is based on a belief that skill will be able to move cash between higher returning opportunities. That skill may can come through finding alpha with individual securities or adjusting dynamically beta exposures. The third way will have to be based on greater manager skill since tailwinds will not be present.