One of the core strategies for portfolio diversification is increasing exposure to international stocks and bonds. This risk reduction strategy is easy to achieve, yet the value of this asset class diversification has diminished over the last few years. The financial cycle has more commonality as measured through times series analysis, and it is harder to achieve the diversification benefits desired if there are more correlated financial cycles.

There are many reasons for this increase in the correlation between financial cycles, but no one explanation can fully explain it, even after accounting for the financial crisis.

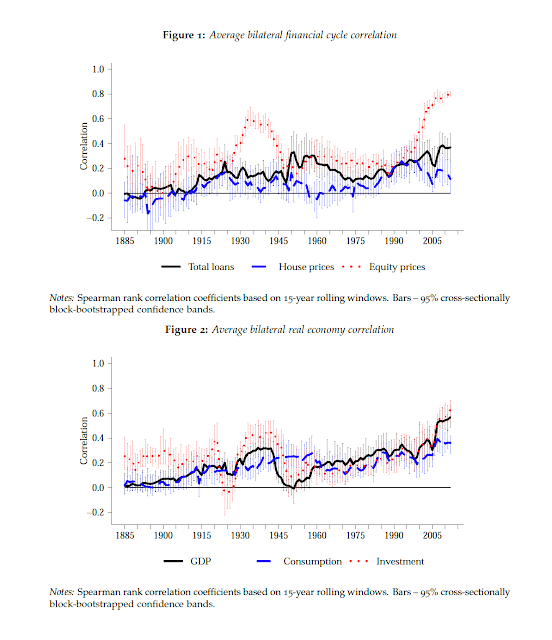

There is a fundamental economic reason for the higher financial correlation; bilateral GDPs are also increasing, but that does not nearly explain the more explosive increase in equity price bilateral correlations. Given the lower capital control, increased capital flows, and greater economic integration, there are structural reasons for bilateral correlation changes. However, the most important may be the tighter financial links between US monetary policy and global risk appetites across countries.

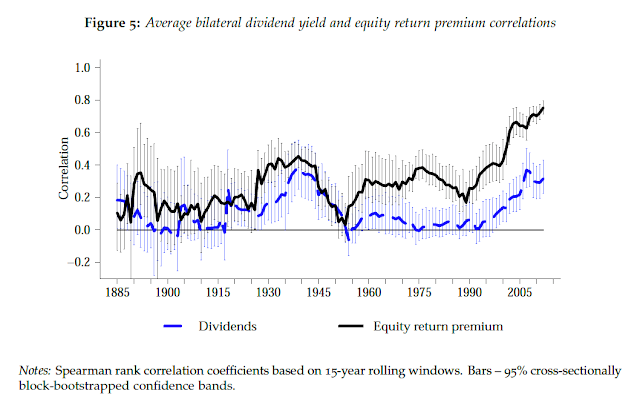

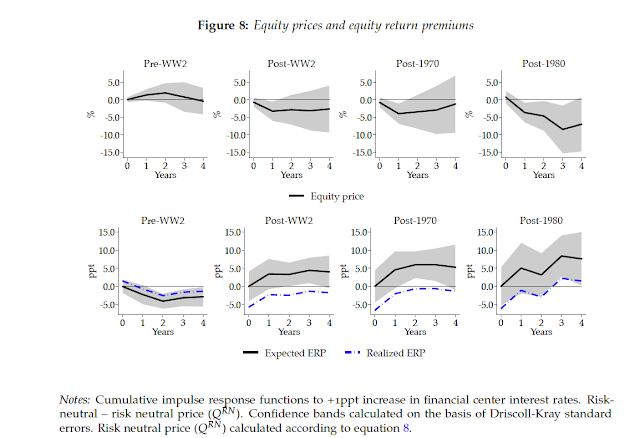

The paper “Global Financial Cycles and Risk Premiums” provides a wealth of empirical information on this critical topic. It shows an apparent change in equity premiums’ response to an interest rate shock over the last few decades.

If this work is accurate, we should see equity prices decline with the Fed’s higher rate policy. Holding risky assets abroad will not provide safety, as global risk appetites change with monetary policy tightening. Investors will have to look harder for diversification in their portfolios.

Given the lack of diversification from equity risk premiums, investors will have to look to alternative risk premiums to gain diversification based on factors less sensitive to risk appetites. This may not be easy since attitudes to risk pervade all risk premiums.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]