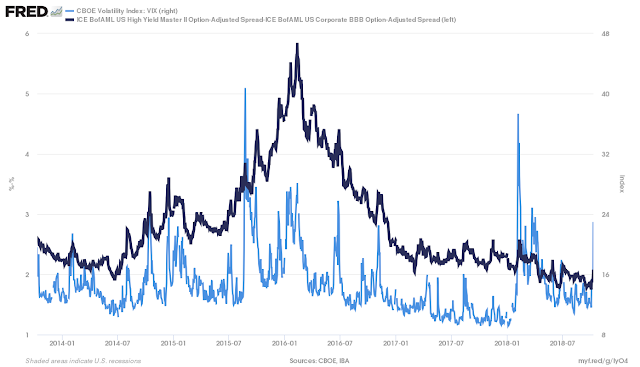

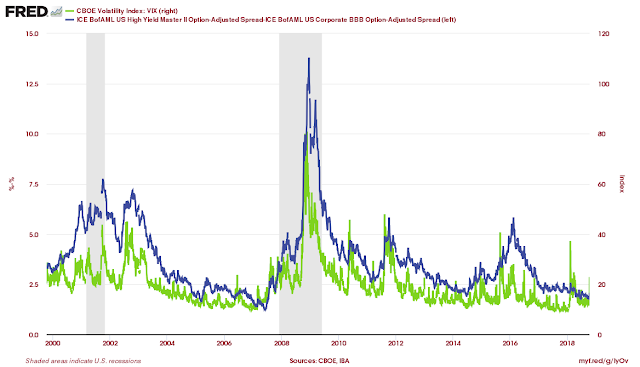

Volatility has spiked higher with the decline in equities, but there are also volatility effects on other markets. Using a Merton debt framework, corporate bonds can be thought of as a risk free bond and a short put position on the value of the firm minus its liabilities. Hence, if market volatility increases as measured by the VIX, there should be an increase in corporate spreads. Additionally, the spreads should increase more for highly levered firms or firms that have higher risk such as those represented in the high yield market. This increase in spreads is related to the increase in the volatility of the value of the firm and not the volatility of interest rates or call features which will be incorporated in the option-adjusted spread.

Looking at the spread between high yield and BBB bonds through the BAML bond indices shows that recent volatility spikes have translated into wider spreads. This spread widening on spikes has generally been temporary and revert with volatility declines but longer-term increases in volatility do translate to higher sustained spread levels. Corporate credit may not be as safe as evidenced in recent data if volatility stays higher.