Emerging markets were talked about in many 2018 forecasts as the place to increase allocations both for bonds and stocks, yet that recommendation has been a performance disaster for many investors. For both the last year and for longer investment periods, EM has not matched the performance of DM equities or bonds. The current causes are many: trade wars scares, low commodity prices, a strong dollar and currency crises, over leverage, slower recent growth, and some strong geopolitical blow-ups. There are strong risks present, yet the arc of economic progress and convergence is still in place for those who think in the long run.

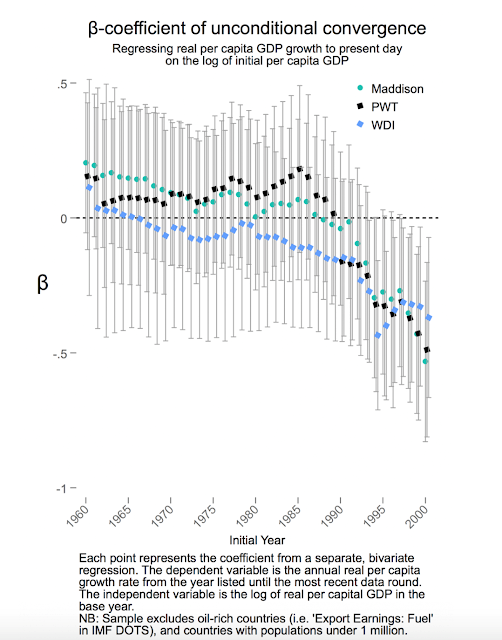

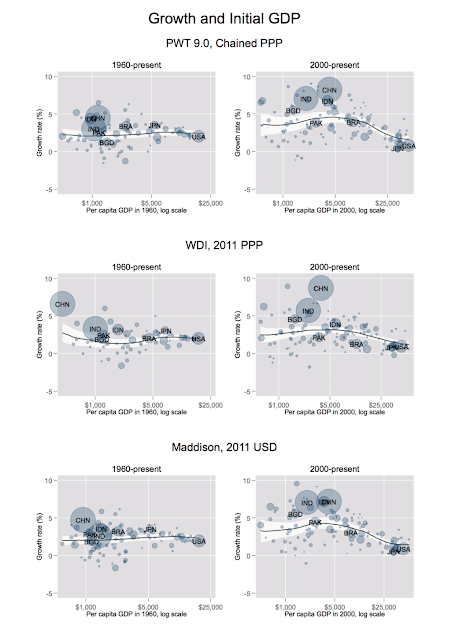

There are many reasons to support EM investing but one of key long-run reason is the convergence of economic growth. The gap between EM and DM income levels is closing and will continue to close. For example, see the latest work on growth convergence, “Everything you know about cross-country convergence is (now) wrong”. A standard view is that the middle-income countries have a hard time continuing high growth. Thus, the convergence of real per capita GDP is harder to achieve. The recent data does not support this claim.

This convergence means that EM will still be a place where sales will grow and will be an increasing share of earnings. Perhaps the place to invest will be through multi-national firms that have committed to EM, but this income gap convergence will not end and EM countries are still a place for opportunity. On a tactical basis, an EM investment may not be this month, and investors may have to be more selective than just buying an index, but the tailwind from growth is a trend that every investor should support