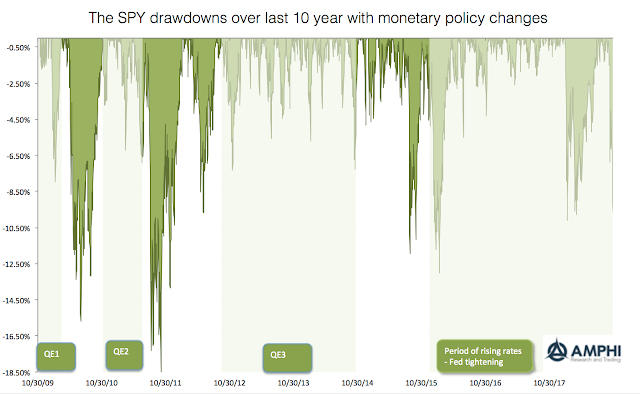

Our graph looks at the drawdowns for the equity benchmark SPY over the last ten years. While the current drawdown has come fast, there are have been a number of drawdowns that have been far worse albeit none that have reached the magic 20 percent market correction level. There is reason to be concerned, but investors need to have perspective.

Nevertheless, we have noticed that the largest drawdowns were associated with periods when the Fed was not generating more liquidity. During the transition period between QE1 and QE2, there was a 15% drawdown. During the transition period between QE2 and QE3, there was an 18+% drawdown. The next four largest drawdowns occurred after the Fed stopped quantitative easing. The periods of quantitative easing were drawdown exceptional because there were no large drawdowns. We are now in a more normal environment, more risk, larger drawdowns, and more uncertainty.