There has been a lot of discussion on the lack of success with momentum and trend-following strategies. There is little doubt that there has been greater dispersion in returns across managers. There have been winners and losers with disappointment focused on some larger high profile firms.

Small differences in models have lead to large changes in return. This is what happens when momentum is not smooth. Smoothness is defined as the trend to volatility ratio, or the switching of return patterns for classic momentum filters. Nevertheless, the strategy is sound. Just look at a simple momentum strategy over a relatively difficult year.

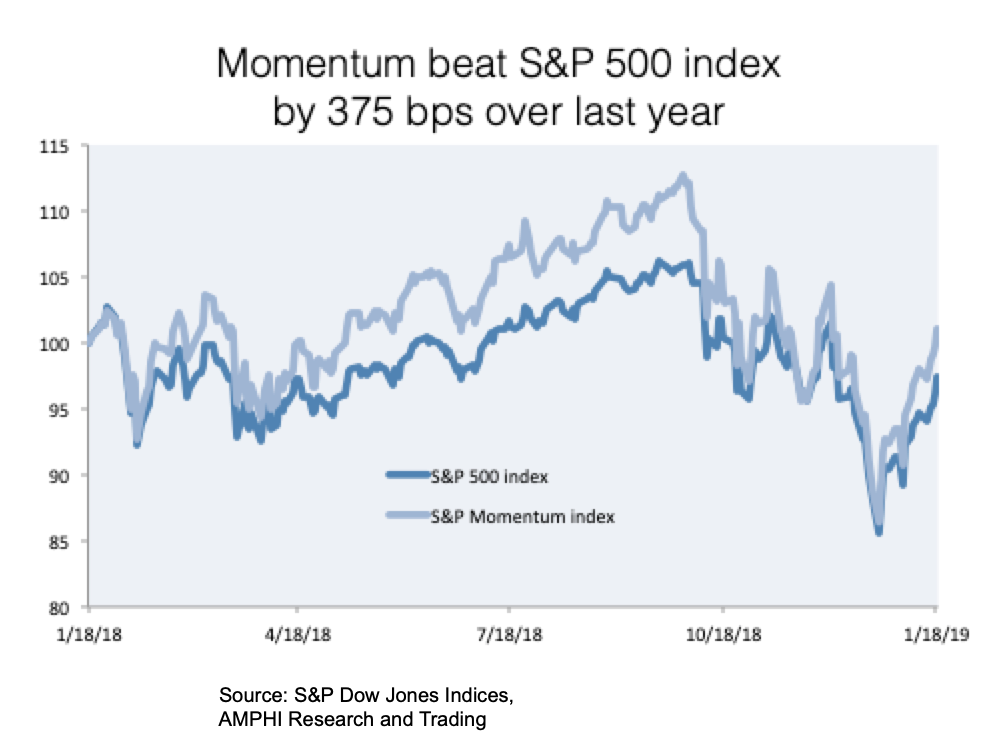

This SP/Dow Jones momentum index, using the large cap 500 equity set, is compared with the SPX index. The overall return impact has been positive over the last year. Clearly there are some expected patterns between the two indices. One, when the market trends in one direction, momentum will exaggerate the market direction for the better and worst. Two, momentum reversals lead to givebacks versus the market weighted index. Three, a long-only momentum index will exploit the long-term positive equity direction. Four, there is a cost with momentum, higher volatility and a return penalty during transitions.

Momentum strategies work, but part of the risk premia for holding the strategy is the cost of transitions. Investors who are late entrants to a momentum strategy will face the highest risks. Momentum should be a core part of asset allocation or entry for this risk premia exposure should be during periods of poor performance. Timing on superior past performance is risky.