Mark Rzepczynski, Author at IASG

Prior to co-founding AMPHI, Mark was the CEO of the fund group at FourWinds Capital Mgmt. Mark was also President and CIO at John W. Henry & Co., an iconic Commodity Trading Advisor. Mark has headed fixed income research at Fidelity Management and Research, served as senior economist for the CME, and as a finance professor at the Univ. of Houston Baer School of Business.

Yield Curve Impact on Asset Prices – Evidence Does Not Provide Simple Answers

Let’s just make things clear. There have not been many yield curve inversions, so analysts who want to study the behavior of asset prices during inversions have limited data. Yield curves may signal recessions which may also signal a decline in equities associated with slower growth, but the timing links are highly variable. The risk differs depending on how the question is asked.

Central Bankers as a Tribe of Technocrats – Outside the Mainstream?

Are you a technocrats or a politician? If you listen to central banks, they will say they are just technocrats or experts who do not engage in politics. To discuss political implications of policy or have politicians involved in the discussion is an infringement on a central banker’s cherished independence. Only through independence and limited oversight can central banks do their sacred technical work.

Managed Futures Funds Not Able To Find Trends

This was a negative month for managed futures funds as measured by peer indices for a simple reason, range bound behavior in equities and a reversal in bonds. Equity indices have started to trend higher, but longer-term trend followers were not able to effectively exploit these moves in the second half of the month. Global bonds have trended higher for most of the month but smaller position sizes based on higher volatility limited gains. Oil prices offered strong gains, but the size of positions may not have large enough to make an overall impact on fund returns. Commodity trades are generally a small portion of the total risk exposure for large funds.

French Political Uncertainty Not Priced Effectively

The cost of being wrong with political uncertainty is significant and the impact will be felt across many markets. The yellow jacket “uprising” has already shifted French economic policy and will also affect the direction of government. We may not be extremists but the fundamental pact between the governed and government is broken which is not good for any investments.

November Performance – Bonds Say Environment Is Negative, Equities Don’t Agree

Last month nothing worked with all asset classes generating negative returns. October saw a shift in market sentiment toward risk-off behavior. Investors started to take loses and adjust to more defensive portfolios. Momentum was clearly negative early in November, but monthly returns are sending different signals with both US and global equities higher. Nevertheless, it is too early to make any statement that risk-taking is back on. Equity markets have come off lows but are not showing any trends. Credit ETFs declined sharply relative to Treasuries and long duration bonds gained on new fears of economic slowdown. Commodities declined on a sharp fall in energy prices.

The Illiquidity Dilemma: Navigating the Risks of Alternative Investments

If you have an asset that has an illiquidity premium, an optimizer will love it as a choice. An illiquidity premium is a dangerous area for investing. First, are you getting paid enough for illiquid? Second, is there a good way to measure illiquidity? Third, do you really know your liquidity needs?

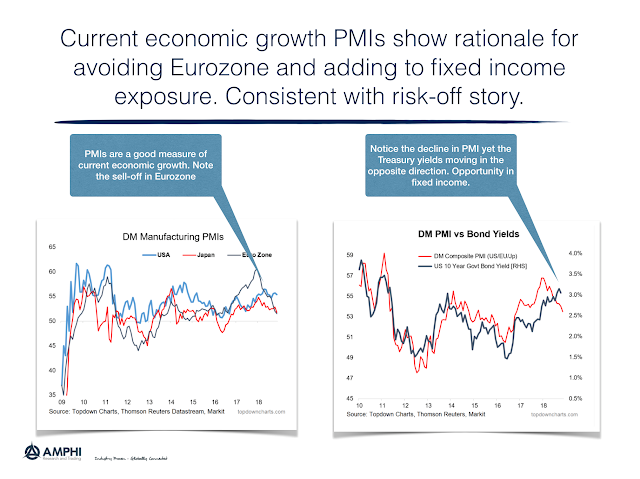

What is PMI Telling Us about Stock/Bond Mix?

A big problem with macro fundamental investing is getting timely data on the economy and then translating that information to effective investment signals. Government issued data generally are out of date and old information for forward looking forecasts. Hence, there is greater value on macro data that is current and prospective.

Can You Improve on the 60/40 Stock/Bond Allocation Without Changing the 60/40 Allocation?

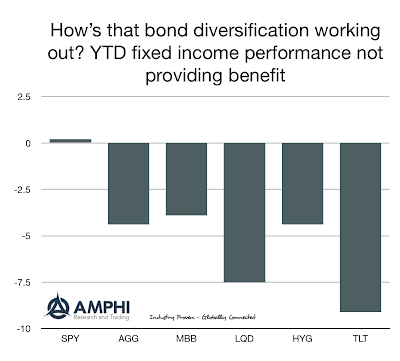

The classic 60/40 stock bond asset mix has proven to be a good core asset allocation. When in doubt, employing the simple 60/40 (SPY/AGG) asset mix as a base case has been an allocation that has performed well versus other diversification strategies. This allocation bias may be coming to an end.

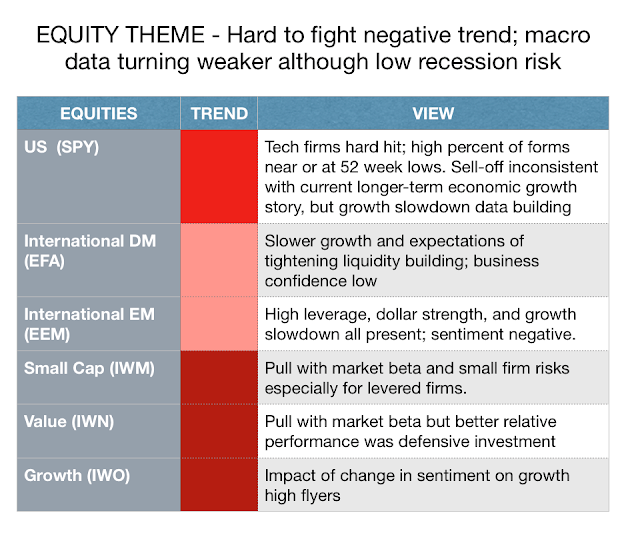

Equity Risk Allocation – No Change in Exposure Reduction View

It not a matter of like or dislike the fundamentals of equities in the current environment. When sentiment changes and volatility increases, reassessment of current exposures is warranted. However, concern about the macro environment should be increasing. Maintaining lower market risk exposure by more than half of core allocation from 60% to 30% or half equity beta exposure is appropriate. (The darker red signifies a stronger trend.)

Categorization and Classification – Fundamental to Finance and Investing

“Categorization is not a matter to be taken lightly. There is nothing more basic than categorization to our thought, perception, action, and speech. Every time we see something as a kind of thing… we are categorizing.”

– Linguist George Lakoff

From The Geometry of Wealth by Brian Portnoy

Most investment work is about forming categories. We divide securities into asset classes. We make subcategories within an asset classes. We make industry classifications. We divide risks into different types of premia. There are value classifications. There are categories and classifications based on macro factors like inflation. Investors like to group. All scientists like to make groups and form clusters of similar things to find commonality.

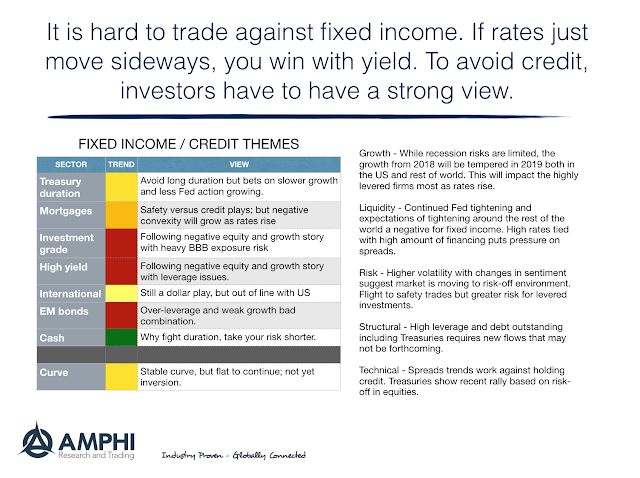

Fixed Income Choices – Move To Further Underweight

Current views on asset allocation in fixed income and credit are generally negative. The focus should be on holding shorter duration and cash investments.

Spread Widening Can Be Costly – All Is Not Well In Credit Land

It does not take much for an investor to have a losing credit trade on long duration bonds. The average duration on a long-term 10-year corporate is around 8 and current OAS spreads for triple-B corporates are 160 over Treasuries up from 120 earlier in the year. Half this move will take investors back to levels seen in 2016 and wipeout all of the spread compensation for a year. This is not an extreme bet if we have any further erosion of equity prices or change in credit risk expectations, (See Corporate debt growth has exploded – The added macro shock sensitivity creates real risks.) Shorter duration corporates will be at less risk given their lower duration but the stocking up of credit for yield reaching can be painful if credit risks increase.

No Diversification in Mudville – Time To Try Different Risk Premia Styles

Diversification is usually thought of as a longer-term concept. Don’t worry if it seems like you are not receiving diversification in a given month or quarter. Think about diversification across a longer horizon. Diversification also does not guarantee better returns for a portfolio. Negative diversification does mean that your losers will be offset with winners.