Category: Uncategorized

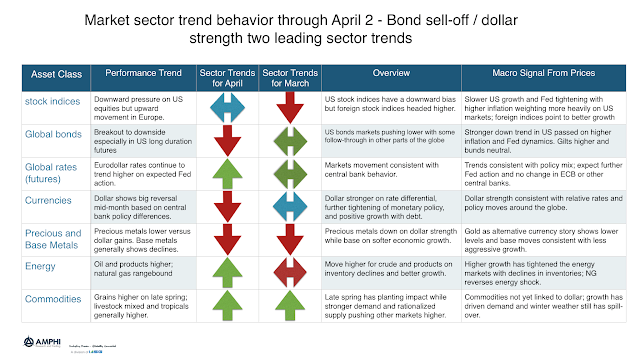

The Sell-Off of Bonds and Dollar Strengthening are the Two Leading Trends Expected for May

Our sector trend indicators, a combination of different trend length directions added across markets within a sector, show some significant changes from last month. This represents opportunities for May but also why some managers showed mixed performance for April.

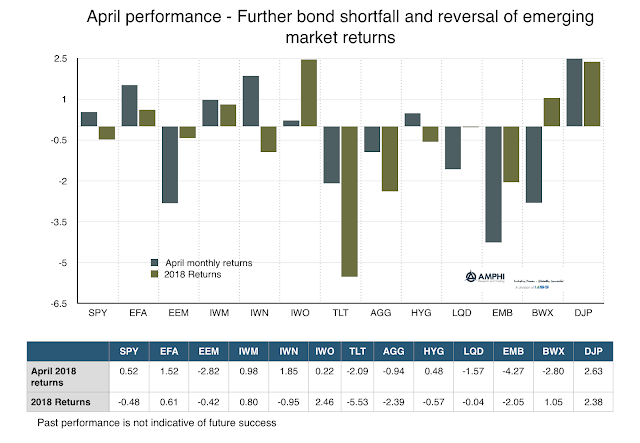

Call It the Revenge of the Safe Asset – Bond Returns Decline

Call it the revenge of the safe asset. Bonds, especially on the long-end, continue to see a sell-off on a surge in inflation and the continued view that the Fed will not change their rate hiking program. This decline has been coupled with generally weaker performance in equities which has led to higher correlation between equity and bonds. The correlation measurement, which is backward-looking, still is negative between stock and bonds but it has risen from previous lows. This increase reduces the “safety” effect associated with bond diversification which has been the “free lunch” for many investors. This will be a growing problem if it continues. Investors will have to make portfolio diversification changes.

Improving Global Macro Investing – Monitor and Understand Financial Conditions both Globally and Locally

What is the most fundamental lesson learned for investors from the Financial Crisis of 2008? It is simple and in the name. We don’t call 2008 the Great Recession. We call it the Financial Crisis. Financial conditions matter more than what we have thought in the past. If money and credit is the oil that runs the engine of commerce, then financial conditions measure the efficiency of the wiring.

The Battle with Ambiguity – It is Constant within Investment Management

…Choices in situations of extreme uncertainty, which I termed “ambiguity”: sparse information, unprecedented or unfamiliar circumstances, lack of reliable frameworks for understanding processes, conflicting evidence of testimony, or contradictory opinions of experts….I felt that existing theories of appropriate behavior (“rational choice”) in these circumstances were inadequate, in fact misleading…

There is Value in the Bundle – Blending Alternative Risk Premiums – The Two Key Advantages

There is a host of alternative risk premiums that are available in the market; some have low returns and low volatility, some good returns but low information ratios, and others have had spotty returns that have moved between good and bad periods. Yet, there is a significant value with these strategies when they are blended together through total return swaps. The value is created through two key features, the low correlation across strategies and the executing through swaps which provides variable leverage.

Risk-Taking – Is it Nature or Nurture? – You May Not be Able to Escape Your Past

Why are some investors risk takers and others are not? Is risk-taking something that can be taught or is it innate? Risk-taking – is it nature or nurture?

The Yield Curve is Flattening – What is it Telling Investors and What Should You Do about It?

There has been a litany of stories on yield curve flatness as if this is the signal that will provide the investment secret to success for 2018. Investors should watch the yield curve closely, but it is important to focus on what it is and is not signaling. There is a cost with trying to be preemptive to what is being signaled in the yield curve.

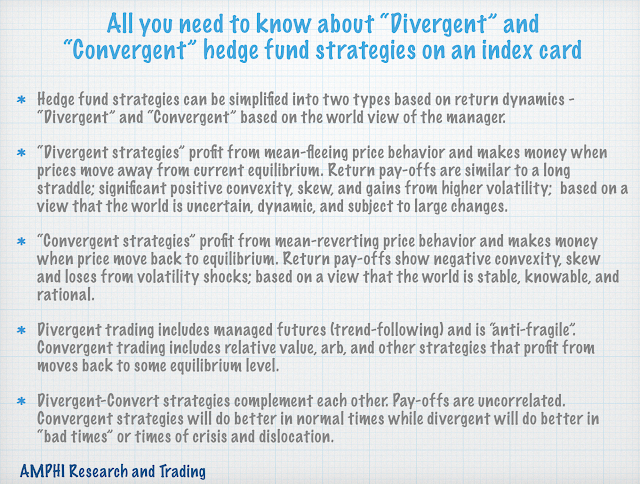

The “3 by 5 Index Card” on “Divergent” and “Convergent” Hedge Fund Strategies

This is the second in our series; all you need to know about a topic should fit on a “3 by 5” index card. We think the complexity of hedge fund investing can be simplified if the simple dichotomy of divergent and convergent trading is used as a primary method of describing potential return pay-offs.

Option Strategies Over Hedge Funds – Why Not? The Number Tell a Good Story

There has been a consistent drumbeat that investors should use hedge funds as a core means of portfolio diversification. This has been at the expense of other methods of hedging. A diversification strategy makes sense when there is no investor information advantage or no view on the direction of markets, but in reality, investors often have some view on market direction or risks at the extreme. However, given the uncertainty on market direction and the inability to form conditional hedges, the investor focus is usually on strategy diversification through hedge funds.

Speculators and Commodity Markets – The Data Does Not Support a Bias in Prices

Do speculators drive prices away from commodity fundamentals? This is one of the core commodity futures markets questions. One approach to answering this question is through looking at the price dynamics, but the advantage of futures is that we have reporting of position information by specific traders groups. Trade flows can be divided into producers, money managers (speculators), swaps dealers, and indexers. The relative balance between these groups can tell us about the market structure, a dynamic agent-based analysis.

Morningstar Star Prediction – Signal to Noise is Low

Morningstar star ratings – Do they really work or are they a dangerous tool? This is important to revisit given the increased number of hedge funds that now have ’40 Act fund structures that are ranked by Morningstar.

What Should You Get with Complexity in Beta Strategies – Smoother Return to Risk

There has been an explosion of alternative measures and methods to access market betas and risk premiums, yet it is not always easy to explain what this added complexity should give investors. We want to simplify the discussion to a simple trade-off – added beta “complexity” through either decomposing, diversifying, or managing the set of betas should reduce the range of return to risk.

The Evolution of Trend-Following Firms to Alternative Risk Premiums and Quant Shops

Trend-following CTAs and managed futures has evolved over the years. Many of the largest firms today would not be recognizable from those who were the largest during the 1980s and 90s. Some of this change in leadership is due to business decisions, but it also has to do with the evolution of the investment process. CTAs have evolved with research trends in finance, the changing focus of overall money management, technological developments, and structural changes in markets.