Category: Uncategorized

Buy in a Drawdown? Focus on Future and not the Past Performance

Managed futures, as a hedge fund strategy, have moved off of its max drawdown since June, its worst drawdown in the last five years, as measured by the SocGen CTA index. For some investors this type of drawdown means an exit from the strategy; however, some of the broader data on manager selection suggest a different approach. The idea of being careful about making investment decision based on a drawdown is consistent with the mean reversion performance analysis of winners and losers.

Not Buying the Fed Package – The Fed, Yield Curve, and Bonds

The take-away quote from Yellen this week, “The relationship between the business cycle and the yield curve may have changed.” There was little supporting evidence for her view. It is the hope of the Fed that further rate increases which may further flatten the yield curve will not reverse the current course of the economy.

Producing Alpha Is Not Easy – The Solution to Making Effective Decisions in an Uncertain World has not Been Found

“What I think HBS does and does very well is train people to, in situations of ambiguity, to take imperfect information, uncertain outcomes, and tight deadlines and figure out what to do in the most effective, efficient, and powerful way.” – Casey Gerald from The Golden Passport: Harvard Business School, the Limits of Capitalism, and the Moral Failure of the MBA Elite by Duff McDonald

Financial Conditions – No Signal of Tightening. Trend Says Stay the Course with Risky Assets

The Fed has become more focused on financial market conditions since the Financial Crisis. There is less interest in the classic goal of managing full employment since by many measures we may beyond the natural rate of full employment, and there is admitted confusion on how to control inflation.

Equity Asset Class Value Rotation – Look Outside the US for Upside and Protection

The talk has focused on the overvaluation and “bubble” with US stocks, but there are other relative opportunities in risky equity assets. A comparison of CAPE across the world shows that the UK, euro area, and Japan valuations are closely tied together, significantly below highs from 2008, and all relatively cheap versus US.

“Risk of a Rapid Repricing in Global Markets” – (ECB) With this Narrative, Investors Need Strategies that Generate Portfolio Gamma

“Risk of a rapid repricing in global markets”; this ECB quote was a key talking point in the press release from the ECB Financial Stability Report issued last week. Note that “rapid repricing” is a polite way of saying asset price declines.

Hedge Fund Performance Mixed, but some Bright Spots with Fundamental Growth and Systematic Macro

Hedge funds returns were mixed for November, but the fundamental growth and systematic macro strategies generated strong returns of over 1 percent. The fundamental growth strategy is the HFR leader for the year with a return profile at over 17%. The macro systematic strategy again generated a strong positive return. The HFR macro systematic index return was significantly higher than other systematic indices for November which suggest a high dispersion across managers in this category. The macro/ CTA which includes discretionary managers was actually down for the month. The absolute return, special situations, and emerging markets strategies were the biggest down strategies for the month, but all showed declines of less than one percent.

Sector Return Performance for Equities Strong across the Board – Hold Overweight in Equities

Equity style sectors were strong across the board with only emerging markets posting a negative November return; however, emerging markets have been the best performing sector year to date. The value index showed a strong gain although it still lags the growth index year-to-date. Trend indicators are all positive except for emerging markets and the short-term trend in the small cap index. Price indicators suggest that there is no reason to cut equity exposures.

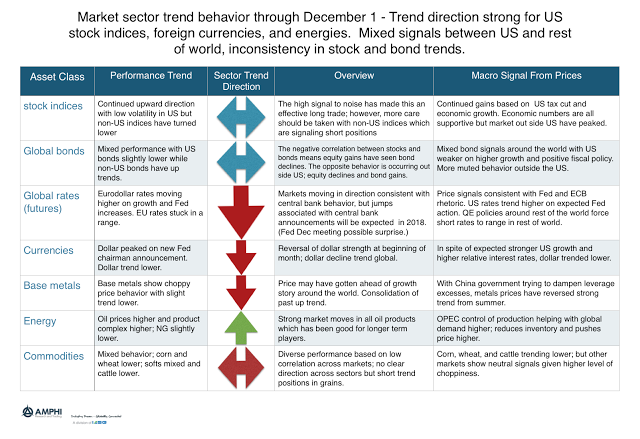

Trends Signals Still Mixed in Many Asset Classes – Long US Equity Indices Still Strongest Signal

Trend behavior last month was mixed for many CTA managers. The allocation weights had a significant impact on November performance. We believe there may again be significant dispersion in performance because trend dispersion is high. For example, US stock indices show strong up trend signals while non-US stock indices are showing clear short signals. The opposite is the case for bonds where US bond signals are for short positions while non-US bonds signals point to long positions.

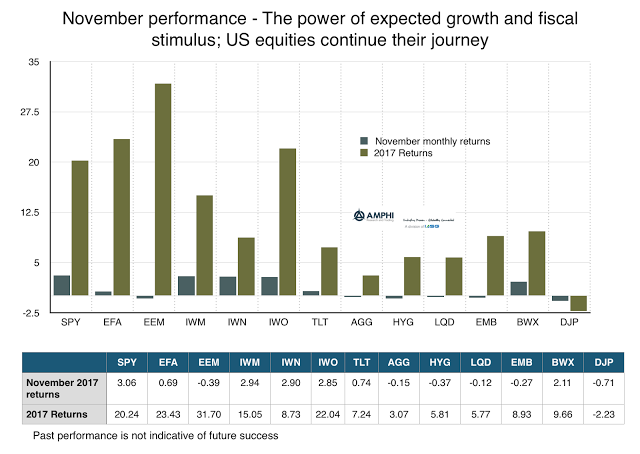

Stocks Continue Their Strong Performance – Hard to Fight Equity Trends; The Opportunity Cost of not Following Trends is High

A combination of good economic growth news and a fiscal policy tailwind again drove US equity markets. The discounting of a US fiscal accelerant shows up in the positive US-global return differential for the November.

Expected Yields and Returns for Bonds are Still Low – Go Get More Alternatives

The asset allocation decision concerning the addition of alternative investments, especially for diversification strategies, is actually quite straightforward. One, find strategies that have low and stable correlations with stocks and bonds. Two, find strategies that have a minimum acceptable return that will beat a traditional diversifier.

Normalcy for Stock Bond Correlation Says You Need Other Forms of Diversification

The bond diversification story is based on the strong negative correlation between stocks and bonds that has existed for over a decade, yet it is not a given that stocks and bond returns will move in opposite directions. A quick look at a very long history from a Wellington Management chart tells us that the negative correlation is the exception not the rule.

Strategic Asset Allocation – Adding Value in a Low Returns Worlds

Strategic asset allocation as the name implies requires long-term return assumptions. There are often wide variations in the future forecasts. Many forecasts we have surveyed show positive expected returns, but the numbers are significantly lower than what investors have seen historically since the Financial Crisis. In general, Research Affiliates provides a good tool for analyzing the past and expected returns that we find helpful.