Category: Uncategorized

News Sentiment – It is Worth Following

Some may feel they are overloaded with news and it is just noise. Well, some new machine learning research suggests that following new is worth a second look. The news can provide a strong measure of sentiment that can improve forecasts versus using traditional fundamental information. This news sentiment is also unique and can add value versus survey sentiment information found in the long-serving Conference Board and University of Michigan work. This new research on sentiment is presented in the paper, “Measuring News Sentiment” from the Federal Reserve Bank of San Francisco.

Bond and Equity Flows -Who is Underwater?

Asset allocation changes are often associated with the pain faced by investors. When there is financial pain through loses, allocations change, so it is important to know where are the pain points. Pain points can be associated with book value loses. Look at when money flowed into an asset class and the price associated with that flow.

BlackRock Survey – Investors Will Pour Into Real Assets

Earlier this month, BlackRock reported their institutional investor survey findings taken from late last year. The results are not that surprising if you believe that inflation may be rising and there is still a need for yield. Cash levels are expected to decline along with fixed income, but real estate will see a large boost. Investors will reduce public equity exposure, but increase their exposure to private equity. There is a bias to less liquid higher risky assets. What may catch some by surprise is the large increase in allocations to real assets which includes timber, commodities, infrastructure, and farmland.

Endowment Models – Bogle Simplicity a Winner

Everyone likes to follow what endowments are doing because there is the assumption that they represent smart money. If universities are where the smart people are, then it stands to reason that their money managers are also smart. The return numbers suggest that endowments don’t have a lock on good performance. In fact, simple allocations have proven to be more effective at generating return. The Bogle model which is a simple variation on the classic 60/40 stock/bond mix is a perfect example. This asset allocation in made up of 40% US equities (total US stock index), 20% international equities (total international stock index) and 40% bonds (total bond index). The Bogle allocation works when compared with endowment allocation which have been tilted to alternatives and away from equities.

Hedge Fund Performance Starts Well for January

The markets were generally calm for January even with the upheaval and uncertainty from the new Trump Administration. The surprise for many investors is the continued low volatility in the markets which seems inconsistent with the political uncertainty faced. While hedge funds generally did well for the month, there were some negative stand-outs, the macro and CTA strategies.

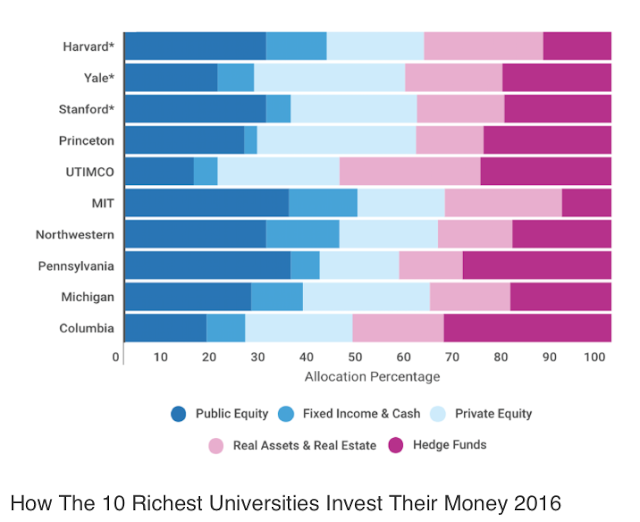

What are Endowments Doing with Their Allocations?

This above chart from thetrustedinsight.com provides an interesting tale about asset allocation for large endowments. Forgot about the traditional 60/40 stock/bond mix. Forget about the 50/30/20 stock/bond/alternatives mix. If you don’t need liquidity, as is the case for the endowment portfolio allocations, a mix between liquid and illiquid is a better base framework. Hold private equity and real estate as core allocations. This core is for long-term appreciation and cash flow greater than bonds, but is generally illiquid. Take money from fixed income and cash. Take funds from public equities and use hedge funds, which may have mixed liquidity, as an additional return enhancer. The public equity and bond/cash portion of portfolios is between 25 and 50%, while hedge funds are from 7.5 to 32.5% for these key endowments. The majority of their allocations are not with traditional equity and bond beta.

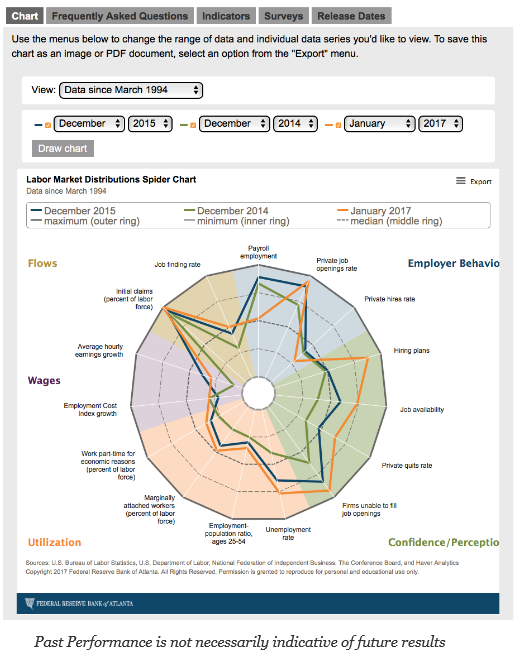

Labor Spider Shows the Key Issues – Utilization

There are a lot of labor statistics to analyze to measure what may happen with fed policy and interest rates. One of the key problems is trying to place all of this information on a single page or in a visual format that can do proper comparison with the past and provide analysis of the present. The Atlanta Fed has achieved that goal with their new labor spider graph.

Trendless Markets as We Move into February

Our sector indicators have all pointed to more trendless behavior for the major asset classes. The only major trend was a decline in the dollar for January and stronger moves higher for precious metals. With higher inflation expectations, and policy uncertainty, there are fundamental reasons for these moves.

Emerging Markets – Bonds Beat Equities Which Beat Commodities – Will this Continue?

Emerging markets have been a tough place to invest especially in equities during the post Financial Crisis period. We include a stock index (EEM), and bond index (EMB) and a commodity index (DJP) for some simple comparisons of three ways to play emerging markets. After a strong rebound in 2009, emerging market equities have generated no returns for investors. Slower growth, poor commodity markets, and a stronger dollar have left equity holders with nothing to show for seven years. Emerging market bonds have told a different story with strong consistent gains since the Financial Crisis even with the strong dollar move over the last few years.

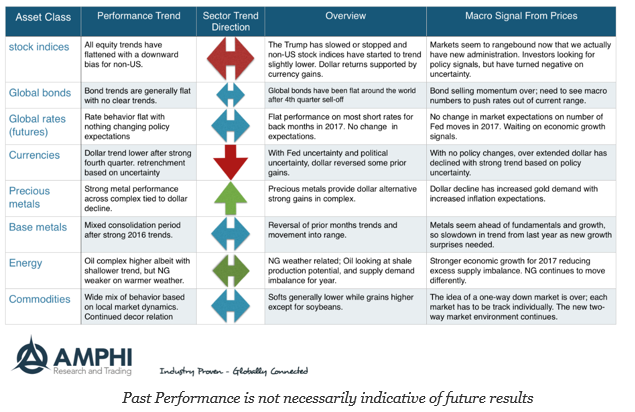

Sector Behavior Shows Stability After Large Moves at End of the Year

It was a positive month for risky assets, albeit more one of consolidation and than return break-out like what was seen last quester. Global markets outside of the US, especially emerging markets, showed large gains after a weak fourth quarter. The dollar gains post-election were partially reversed which added a tailwind to non-dollar investments of about 2%. After accounting for currency changes, developed non-dollar returns are back in-line with the US.

Banking and Speculation – All a Matter of Opinion?

“When as a young and unknown man I started to be successful I was referred to as a gambler. My operations increased in scope. Then I was a speculator. The sphere of my activities continued to expand and presently I was known as a banker. Actually I had been doing the same thing all the time.”

– attributed to Ernest Cassel by Bernard Baruch

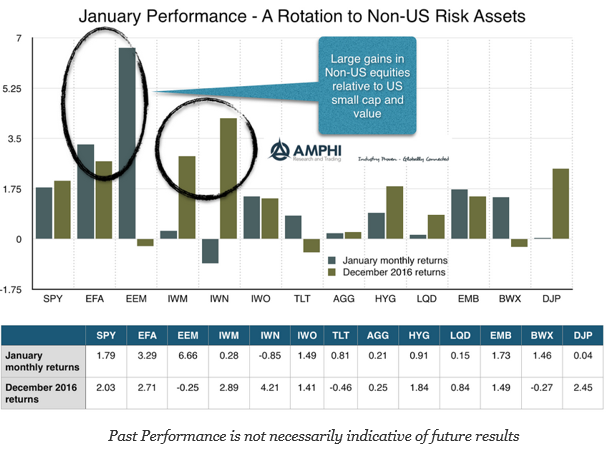

The Switch – An Ascent in Non-US Returns

After the euphoria in small cap, value, and growth stocks post the Trump election, the markets have calmed and moved slightly upwards. Global equities and emerging markets stocks were the big winners for the month. These moves were a degree of catch-up to the outperformance in US stocks. Even with the poor print for fourth quarter GDP, equity investors are discounting better growth in 2017.

Bonds as Diversification Insurance – I Don’t Think So

Would you buy insurance where the value changes every day with market conditions? An “insurance contract” that may provide a hedge against equity risk today only to see the value of the hedge disappear tomorrow? Of course, the value can appear again, but investors may not have any guarantees. This is recent problem of investing in bonds as a diversification tool. The value of this diversification has become more variable.