Category: Uncategorized

Regression to the Mean, Luck and Picking Hedge Fund Managers

There are few statistical facts more interesting than regression to the mean for two reasons. First, people encounter it almost every day of their lives. Second, almost nobody understand it. The coupling of these two reasons makes regression to the mean one of the most fundamental sources of error in human judgment.

-Anonymous from What the Luck? The surprising Role of Chance in our Everyday Lives by Gary Smith

If it Works for Poker, it should Work for Investing…

More money is lost by players who know what the right thing to do is, but don’t do it, than for any other reason. Having a strategy, a game plan and the discipline to stick to it are, along with a sufficient bankroll, the four most important thing that a player needs to be a winner.

– Ken Warren poker writer on Texas Hold ‘Em

Machiavelli Could Have Been a Trend-Follower

Whoever wishes to foresee the future must consult the past; for human events ever resemble those of preceding times. This arises from the fact that they are produced by men who have been, and ever will be, animated by the same passions. The result is that the same problems always exist in every era.

– Niccolo Machiavelli

Downside Risk – Maybe You Should Be an Insurer?

No investor wants to bear downside risk. Well, perhaps more precisely, no one wants to bear downside risk without extra return compensation. Strong asymmetric risk preferences create the reason for a volatility risk premium – the empirical fact that implied volatility is higher than realized volatility. What the volatility risk premium states is that if you buy an option you will pay more in terms of volatility than what the market will give you in actual volatility. In a very simple but elegant paper in the Journal of Alternative Investments called “Embracing Downside Risk”, some practitioners look at the compensation toward downside risk through a decomposition of returns by strategy.

2017 – Living in a Bimodal World

Most investors like to think of financial market risks as measured through a normal distribution. In reality, we know that it is not the case. However, how we incorporate and discuss fat-tails is not always clear. One thing that is clear is that fat-tails can be created when there is a mixed distribution or a combination of distributions that represent different regimes. A simple example will be the mixing of growth versus recession or good versus bad states of the world. This has been our theme for 2017 with a new year post. The potential for two different economic regimes will create fat tails in the return distribution of financial assets.

Money Management – Is the Amount of Talent Important?

Money management is all about the talent, yet there is little economic analysis of human capital as an input in the creation of returns for the money management industry. That gap in research has changed with the new paper, “On the Role of Human Capital in Investment Management”. This provocative paper studies over 10,000 RIA’s across a number of years and asserts that more human capital may not help return generation. Having more advisory personnel may help with attracting assets. More investment advisor employees creates the appearance of more talent, but having more bodies is more likely to generate behavior like a closet index with less active shares and lower tracking error. They call it – money management – and staff is needed for management and the gathering of assets. Investors just have to be careful understanding why more staff is needed.

FX for 2016 – The Betas Say Carry is Back

The development of FX style betas has changed the way investors think about their foreign exchange trading exposure and risks. The approach is simple – trading risks in FX can be decomposed into four style factors, trend, carry, fundamentals, and volatility. The argument states that an investor can easily manage or decompose FX returns using these beta styles or strategies. It is an effective way to show how returns can be generated in currency markets.

Measuring Risks – Working Against the Downside

“I would’ve created CAPM around semi-variance, but no one would have understood the math and I wouldn’t have won Nobel Prize…” H.Markowitz

In a Tough Investment World – Investors Will Need Help Finding Returns

It will be a tough investment world going forward for the simple reason the odds are against you. If you are a blackjack card counter in Vegas, you always know the odds, or the count. You know that on any draw, you can get lucky, but in some environments, the chance of success is just lower. Regardless of how smart you are, if the odds are not with you, your chances of getting good returns are lower. Your job as an investor is to know the odds and deal with the consequences.

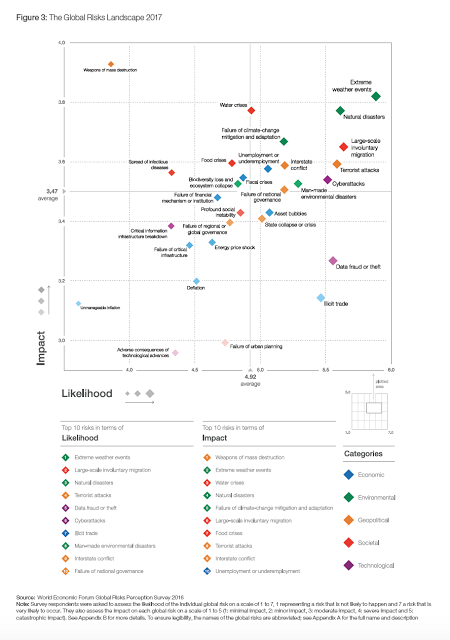

WEF Global Risk Report – What to be Afraid of in 2017

The World Economic Forum (WEF) Global Risk Report serves as a useful guide on the broader set of risks that may impact the world over the next year. This report is important because it moves outside the narrow focus of finance and looks at a broader set of risks. Nowhere are economic issues in the top five for impact or likelihood in 2017. This is a big change from the 2007-2010 period. This is the first time economic issues are neither in the likelihood or impact top five. The dominant category is environmental which suggests that commodities markets are most likely to have the immediate impact if there is a shock. Extreme weather and natural disasters have the highest impact and likelihood combination from WEF analysis

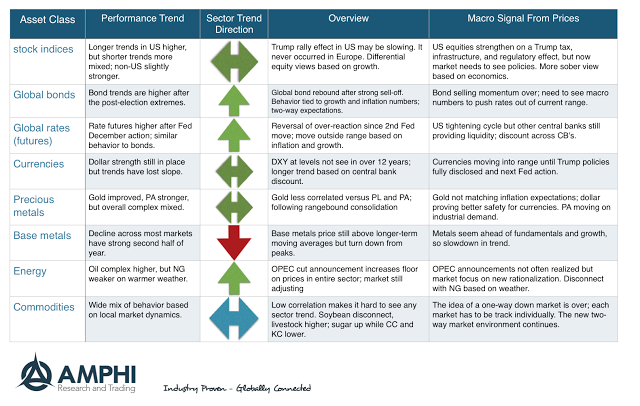

Trends in the Market – The More Cautious Trump Rally

The euphoria of the US presidential election is over. The market jumped under a new wave of optimism associated with an end to fiscal austerity, tax cuts, and regulatory reform, but now the reality has to set in and investors have to see the actual policies and believe they will be effective. This new sense of reality may describe the current price action for asset classes. You can call it mean reversion or a response to an earlier over-reaction.

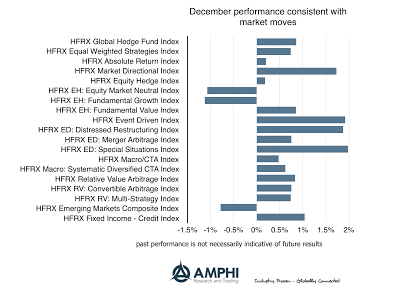

Hedge Fund Performance in 2016 – Was This a Skill-Based Year?

Hedge fund managers are supposed to show skill during periods of higher risk and uncertainty. If there is more uncertainty or ambiguity concerning market, skill-based managers should be able to do better than those who just buy a market index. This is one key reason behind choosing hedge funds. When there is uncertainty and risk, alpha should be generated by skill managers.

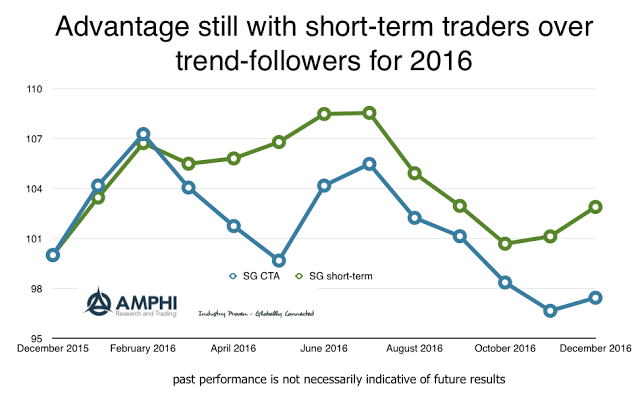

Timing Diversification

All systematic traders are not alike. Investors know that, but the differences become highlighted at the end of the year when returns are reviewed. There are potential diversification gains within a strategy space by choosing a set of managers who behave differently.