Category: Uncategorized

Risk Factors Change – Do You?

From ETF Trends comes an interesting chart on the relative performance of different risk factors for US large cap equities. Factor analysis and building portfolios based on specific factor risks has become all the rage in investing. We think this is useful and significant advancement to portfolio management, but there is still a lot to learn about the dynamic behavior of factors.

Focus – Study on Diseconomies of Scope Demonstrates the Key to Success

We know the answer to success. If you want to get good at something you have to focus and do the work. Is this focus measurable in money management? Similarly, can we say something about manager focus through time? An interesting piece of new research looks at this problem in the paper, Diseconomies of scope and Mutual Fund Manager Performance.

The Buzz with Pension Clients 50-30-20

The rule of thumb used by many investors as a base portfolio allocation has been a 60%/40% stock/bond mix. When in doubt, investors are supposed to go with a standard 60/40 allocation as a safe base case. If you are going to change the allocation, measure the change against the base 60/40 mix. Investors can perhaps add international equity or international bonds or maybe a dash of commodities, but if there is more uncertainty, the safe action is to move back to 60/40. Many advisors may suggest something different, but then show why it would be better than the baseline 60/40 as the reason for its efficacy.

Where do advisers want active management?

There has been a strong move to passive investing tied to benchmarks by investors. The reasons for this movement are threefold. One, passive benchmark investing is cheaper than active management. Two, active management has often underperformed benchmarks. Three, passive investing provides transparency on what will be in the portfolio. Nevertheless, a survey of defined benefit consultants suggest that the choice between active and passive management is not obvious and actually asset class specific. There are some areas where consultants view that active management is important while other areas the focus is for passive investing.

Fidelity Survey – Expect Asset Allocation Changes

A recently published Fidelity Global Institutional Investor survey suggests that more asset allocation changes will be made in the next one to two years than shown in their last two surveys in 2012 and 2014. This survey anticipates what we are all thinking – it is a new investment world with a Fed becoming more aggressive and the politics of populism sweeping many countries. The post-crisis investment world of boundless liquidity and asset performance catch-up has ended. We are entering a new period of two-way market views. There is more uncertainty on market direction so we are likely to see more divergences in asset allocation.

When asked about the top concerns for investing in their portfolios, the three top answers were all boar performance; what is past performance of an asset class, what is the expected return from an asset class, and where has there been success and failure with investments. Perhaps performance is always the top issue in the minds of managers, but the survey highlights particular focus during this period of transition.

Asset Classes, Styles and Sectors Show Dispersion

A review of all sectors shows some clear themes across asset classes. Bonds are out of favor and US equities are preferred. International equities and bonds reflect repricing of rates and currencies while still showing lower global growth.

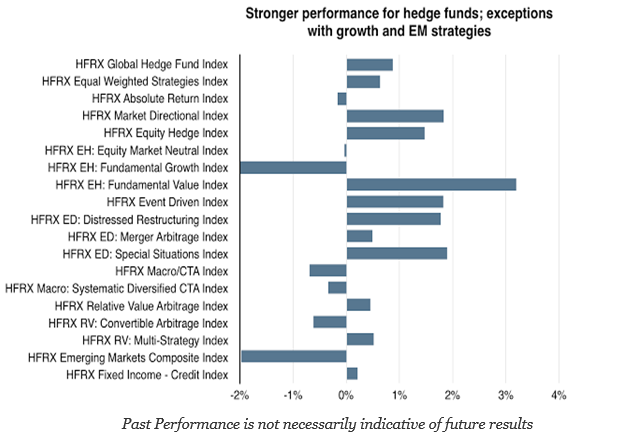

Hedge Fund Performance Stronger but Not Enough to Make a Good Year

A US equity rally after the election and a major bond sell-off highlighted the month for traditional assets. Many hedge fund strategies were able to exploit these moves and generated gains especially in fundamental value, market directional and relative value strategies. The big losers were fundamental growth and emerging markets. Global macro and CTA strategies also generated loses for the month.

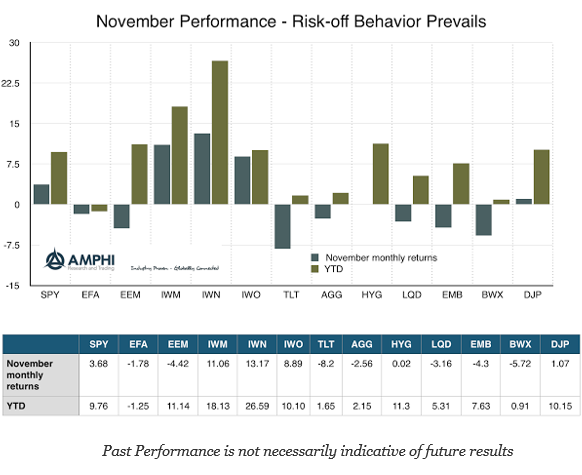

The Big Bond Break and Equity Revival – November Performance

For those who had a “safe” portfolio skewed to bonds before the election, it was a disaster month. For those who were stock-pickers in value and small cap, it was a dream market. The return differential between bonds (TLT) and value (IWN) was more than 20% in one month. Call it a “Trump Rally / Trump Bond Sell-off”, but the financial world changed beyond politics. This sound bite story may be getting old, but there is a lot going on in markets beyond being long stocks and short bonds.

Data Mining – More than Collecting Data Ore

There are fads and fashions in finance and business. Some statistical techniques come and go in and out of favor based on expectations of success and the realization that some tools just cannot solve certain problems. Data mining in now a hot topic in many areas of business, yet there are not clear definitions of what data mining means, what tools it represents, and how it can solve problems. Clearly, the low cost of computing and storage has made the collection of data much easier, but the problem is not with the data. The issue is how you extract the data “ore”, how it is processed, and what you do with it once it is modeled.

Due Diligence of Trading Skill – Can it be Improved?

Being on both side of the table concerning the due diligence of managers, I can argue that there has been a significant improvement with the skill at conducting operational due diligence. Operational risks can be effectively identified and measured. There will be fund failures, but investors can do a good reasonable job of handicapping firm-specific risk. There are checklist and processes that can support the choice of managers. The operational due diligence has been effectively institutionalized.

Old Behaviors Will Have to Change in New environment

“New eras are cut short by the financial behavior they reward and condition,” -James Grant. Too much of anything is not a good thing. Or, as stated by Herbert Stein, “If something cannot go on forever, it will stop.” All investment strategies fail or fall out of style at some point. The financial conditions and […]

Brains and Stomach – You Need Both for Investing

Having the stomach for investing means that you are able to get over the behavioral biases that are based on emotions and fast thinking. It means being able to follow-through with an investment plan without emotions. Meir Statman, a finance professor who has focused on behavioral biases, states, “Deeply buried fears can keep us from taking risk – keeping us safe, perhaps but also robbing us of potential returns. A stronger tendency to regret past choices can keep us from repeating blunders, but also from repeating sound strategies that simply didn’t work out the first time.” from Spencer Jakab, Heads I Win, Tails I Win. Those who have regret have no stomach. Investors who can move beyond regret have the stomach for investing.

Investment Learning Starts with Knowing the Past

I have always had problem with some of the finding behavior finance research. The research is good at pointing out flaws but less effective at offering ways to improve performance and behavior other than stop doing bad things. Nevertheless, I have found some the behavioral research work by Markus Glaser and Martin Weber very helpful with how to offset some biases. They find that there is no correlation between return estimates and realized returns, but they see difference in behavior based on experience. See their work, “Why inexperienced Investors Do Not Learn: They Do Not Know Their Past Portfolio Performance”.