Archives

Warrington Asset Management – Looking back on July

The S&P 500 continued to climb steadily up to the last trading day of the month even though market participants knew that day could bring volatility, as the U.S. Federal Reserve (the “Fed”) was scheduled to announce their latest monetary policy update on July 31st. Speculation about their intentions to lower interest rates for the first time in ten years had been a market focus for months. Fed Funds futures pricing is often used to estimate the probability of pending Fed interest rate changes, and had signaled the most likely decrease to be between 25 and 50 basis points. However, when Charmain Powell announced the 25 basis point cut he also implied it might be a “one and done” scenario rather than a prolonged rate cutting cycle favored by market participants, causing an immediate decline in stock prices. The selling in the S&P was strong, sending the Index to its largest intraday decline since early May. In fact, prior to that drop, the S&P had not had a 1% daily gain or loss in the previous 36 consecutive trading days, the longest streak since early October 2018.

JTM Capital Management – Major Factors Affecting Agriculture

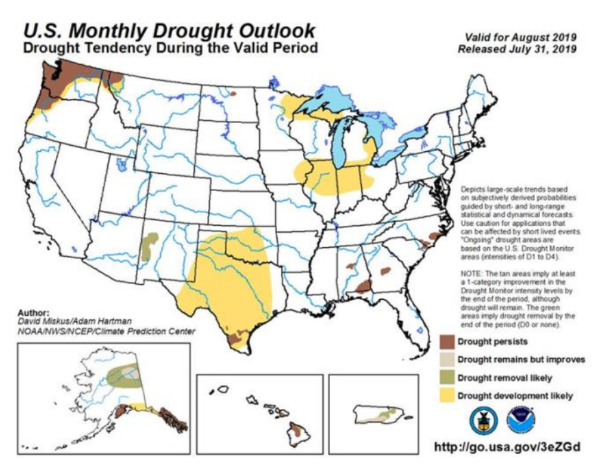

Following up on last month’s commentary, July featured lower than average rainfall and higher than average temperatures across most of the US’s primary growing regions. Interestingly enough these results were quite different than the NOAA long-range forecasts issued for the month. Specifically, most of the Corn Belt experienced maximum temperatures that averaged 2-4 degrees (F) above normal. As you can see on the left even with this year’s extremely wet spring, drought conditions are expected to develop in key growing regions of IA, IL, and IN. This is definitely something to keep an eye on as near perfect conditions will be needed to substantially increase row crop yields at this point.

Third Street AG July Commentary

Data and information is provided for informational purposes only, and is not intended for trading purposes. Neither IASG or Third Street Ag Investments LLC nor any of their data or information providers shall be liable for any errors or delays in the data or information, or for any actions taken in reliance thereon. We do […]

Breakout Funds – Interesting days ahead

What a wild past 27 hours across Macro. Yesterday was one of the most anticipated Fed meetings in memory. Markets were looking for a cut of 25 and hoping for more – either yesterday or in the near future. What we got was 25 and a bumbling press conference where Powell seemed to have no clue what was driving Fed policy at this point. The best we could take away was further trade uncertainty may result in those much begged for rate cuts. But this was just a guess, and that’s the point.

Managing Money: It’s basically all noise, with a few exceptions

Noise and an overwhelming amount of data is the biggest challenge in managing money in 2019 (or anytime in the past decade). In the 1960s, 1970s, and even the 1980s, delivering alpha came down to having access to information others didn’t have – the process of obtaining data was a value-add. Today, we have the complete opposite problem. In 2019 we have too much information, and delivering alpha comes down to paring things back to their essence, stripping away unnecessary garbage.

Why does momentum investing work?

Conventional wisdom says that it should be doomed once any stock-picking strategy nears “sure thing” status. If everyone knows the secret to vast riches, how could the strategy possibly work anymore? But there is a successful strategy that has been followed — and widely discussed — for decades, yet somehow persists as a relatively reliable […]

What does it mean for an investment strategy to be “robust”?

In the business of managing money, there is a key word that often comes up but is easily misunderstood: robustness. What does it mean for an investment strategy to be “robust”? What does a robust strategy look like? Is it something that most investors find palatable? Look at the following returns for two different managers, Mr. low vol and Miss robust.

Sortino: A Sharper Ratio

Many traders and investment managers have the desire to measure and compare CTA managers and / or trading systems. Risk-adjusted returns are one of the most important measures to consider since, given the inherent / free leverage of the futures markets, more return can always be earned by taking more risk. The most common risk-adjusted […]

Trading Palladium: A Classic Macro Approach

Disclaimer: While investment in managed futures can help enhance returns and reduce risk, it can also do just the opposite and, in fact, result in further losses in a portfolio. In addition, studies conducted on managed futures as a whole may not be indicative of the performance of any individual CTA. The results of studies […]

Changing the dynamics of enhanced cash – Switch from credit to alternative risk premia

Investors are always looking for ways to enhance cash returns – higher yield with liquidity and limited principal risk. The timing for using different enhanced cash techniques changes with market conditions. Widening the choice set through investing in alternative risk premia may be a way to meet enhanced cash goals without significantly increasing risk.

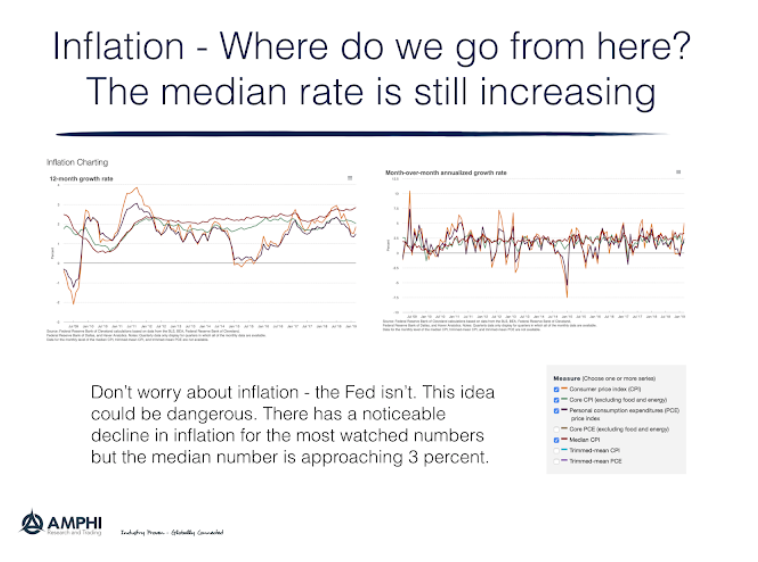

Inflation – Where do we go from here?

Don’t worry about inflation – the Fed isn’t. Or, the Fed believes there is no value is trying to get ahead of any inflation increase given the relatively tight range for inflation. The market penalized any fixed income investor that acted on inflation fears. Any Fed objective function has a higher weight on growth.

Mike Lombardi, football coaching and investing

I am not a football fanatic, but I picked up this book on a recommendation and was amazed by Lombardi’s insights on leadership and management. Mike Lombardi is long-time football executive and media analyst. The book focuses on Bill Belichick and the New England Patriots, but his conclusions could apply to any money management firm. A good money management firm is successful because it acts like a well-disciplined organization with a common purpose. That is no different than a competitively run sports organization. Lombardi finishes his book with five key recommendations for firm success that are worth presenting in bold.

“The Emeril Lagasse Theory” – Practical knowledge and culture is not often transferable

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.