Archives

Is Investment Management a Science – Use the “Narrativeness” Test

“Narrativeness” may be defined as the quality that makes narrative not merely present but essential. It comes in degrees, and there are narratives without narrativeness. Since the time of Leibniz, Western thought has favored models in which abstract scientific laws would ideally account for everything in nature and society (the ideal of a social science) and in which narrative would therefore be, at best, merely illustrative. But a number of thinkers have presented forceful arguments that such an ideal of knowledge is a chimera. Darwin, Dostoevsky, Tolstoy, and others have insisted in the ineluctable need for narrative because genuine contingency exists and time is open.

The Five “Whys” and Investment Management – Finding the Root Cause

I came across in some old papers the Toyota Industries solution to finding the root cause of problems, the 5 whys. It is a simple and useful tool. Sakichi Toyoda, the father of Toyota Industries, developed this technique to solve manufacturing problems, but it could easily be applied to any investment problem or due diligence issue. Ask why five times.

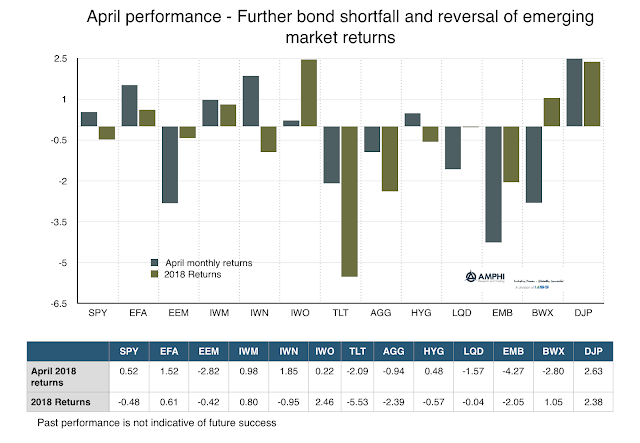

Some Sector Dispersion within Equities but Fixed Income Down Across the Board

There could be a desire to look for special patterns within April performance, but the only clear theme is the risk associated with holding bonds during a rising inflation expectation and tightening Fed environment. These issues spill-over to the dollar which affected affects the performance of international stocks.

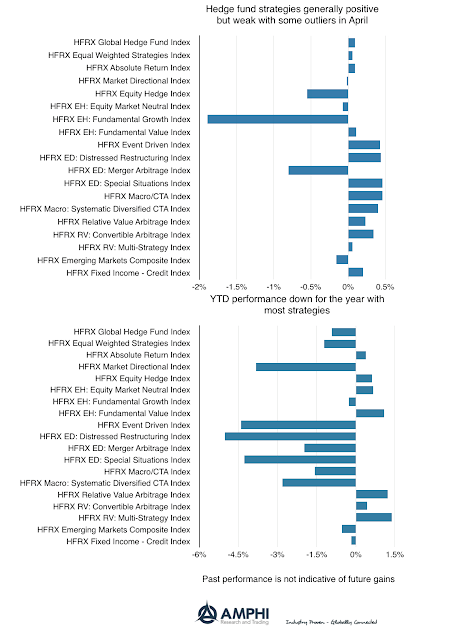

Hedge Fund Performance Positive, but Weak for April – Most YTD Returns Underwater

Most hedge fund strategies were positive for April, but the average return was less than 50 bps. There were two negative outlier strategies with fundamental growth and merger arbitrage. Generally, the higher monthly volatility and dispersion created a mixed environment for return generation. Year to date returns suggest that it has been a difficult four months for most managers with average loses much larger than the average for the winners and only 7/19 strategies producing positive returns.

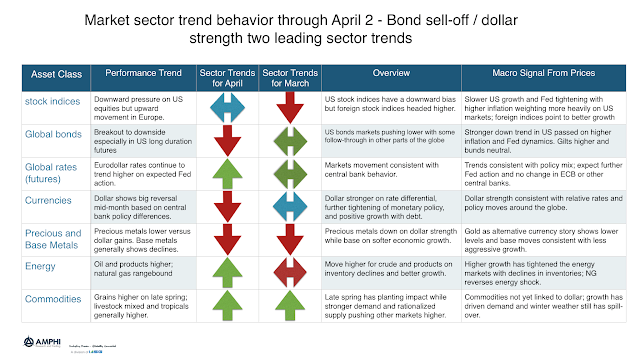

The Sell-Off of Bonds and Dollar Strengthening are the Two Leading Trends Expected for May

Our sector trend indicators, a combination of different trend length directions added across markets within a sector, show some significant changes from last month. This represents opportunities for May but also why some managers showed mixed performance for April.

Call It the Revenge of the Safe Asset – Bond Returns Decline

Call it the revenge of the safe asset. Bonds, especially on the long-end, continue to see a sell-off on a surge in inflation and the continued view that the Fed will not change their rate hiking program. This decline has been coupled with generally weaker performance in equities which has led to higher correlation between equity and bonds. The correlation measurement, which is backward-looking, still is negative between stock and bonds but it has risen from previous lows. This increase reduces the “safety” effect associated with bond diversification which has been the “free lunch” for many investors. This will be a growing problem if it continues. Investors will have to make portfolio diversification changes.

Improving Global Macro Investing – Monitor and Understand Financial Conditions both Globally and Locally

What is the most fundamental lesson learned for investors from the Financial Crisis of 2008? It is simple and in the name. We don’t call 2008 the Great Recession. We call it the Financial Crisis. Financial conditions matter more than what we have thought in the past. If money and credit is the oil that runs the engine of commerce, then financial conditions measure the efficiency of the wiring.

The Battle with Ambiguity – It is Constant within Investment Management

…Choices in situations of extreme uncertainty, which I termed “ambiguity”: sparse information, unprecedented or unfamiliar circumstances, lack of reliable frameworks for understanding processes, conflicting evidence of testimony, or contradictory opinions of experts….I felt that existing theories of appropriate behavior (“rational choice”) in these circumstances were inadequate, in fact misleading…

There is Value in the Bundle – Blending Alternative Risk Premiums – The Two Key Advantages

There is a host of alternative risk premiums that are available in the market; some have low returns and low volatility, some good returns but low information ratios, and others have had spotty returns that have moved between good and bad periods. Yet, there is a significant value with these strategies when they are blended together through total return swaps. The value is created through two key features, the low correlation across strategies and the executing through swaps which provides variable leverage.

Risk-Taking – Is it Nature or Nurture? – You May Not be Able to Escape Your Past

Why are some investors risk takers and others are not? Is risk-taking something that can be taught or is it innate? Risk-taking – is it nature or nurture?

The Yield Curve is Flattening – What is it Telling Investors and What Should You Do about It?

There has been a litany of stories on yield curve flatness as if this is the signal that will provide the investment secret to success for 2018. Investors should watch the yield curve closely, but it is important to focus on what it is and is not signaling. There is a cost with trying to be preemptive to what is being signaled in the yield curve.

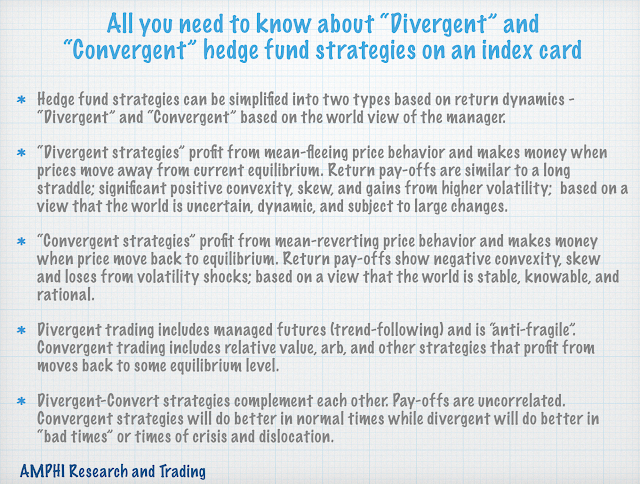

The “3 by 5 Index Card” on “Divergent” and “Convergent” Hedge Fund Strategies

This is the second in our series; all you need to know about a topic should fit on a “3 by 5” index card. We think the complexity of hedge fund investing can be simplified if the simple dichotomy of divergent and convergent trading is used as a primary method of describing potential return pay-offs.

Long/Short Commodity Funds – Adds Value to Equity and Bond Portfolios

Static investments in long-only commodity indices have had a checkered past since the financial crisis. With the end of the commodity super-cycle, there has been a long commodity unwind and passive investing in commodities has provided negative annualized returns for investors for years. There has not been any bounce to pre-crisis level like we seen in equities. The interest in commodities as an inflation hedge has waned with this poor performance.