Archives

Commodity Driven By Global Growth – Above 3% Growth and Prices Push Higher

Commodities are an effective way to hedge against inflation, but it can also be viewed as a simple way to play the global growth story. The average annual total return for the Bloomberg BCOM index (formerly the DJUBS commodity index) since 1992 has been 1.37% but if we look at returns when global growth is above 3%, the average annual return was 10.91%.

Looking Back Over Commodities for the Last Ten to Fifteen Years – Currently in Normalization Phase

Commodities have not behaved like other asset classes since the Financial Crisis. In spite of all the monetary easing and the lowering of interest rates, commodities have marched to their own drummer, or, put differently, the commodity cycle has been independent of the business, financial, or monetary cycles. It is because of this difference that commodity exposure may look more attractive than traditional assets.

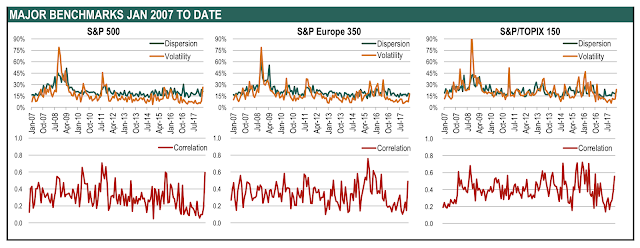

Correlation Up – A Beta Not Alpha World For Now

We follow the dispersion, volatility and correlation indices generated by Standard & Poor’s which show intra-index stock behavior over time. When the correlation across stocks within in an index is high, there is a clear sign that the market is facing a macro shock. Performance should be biased toward beta risks. Fund returns will be driven by their beta exposure and timing skill not by their stock-picking skill. When correlation is low across stocks within an index, we can say it is a stock picker’s environment because skill-based traders will be rewarded for exploiting differentiation across firms. This lower correlation will generate more dispersion in returns if there is additional volatility.

Preqin Investor Survey – What Are The Demands For Hedge Funds?

The recently released Preqin Investor Outlook, Alternative Assets, H1 2018 describes the demanding environment for hedge funds. Investors do not believe hedge fund are meeting their expectations, allocations may be smaller, flows may be reduced, and there is a desire for better alignment of interests. Of course, there is also the desire for more performance. To address these issues hedge funds will have to change.

Pension Asset Allocations – Filled With Alternatives And Not Beta (Willis Towers Watson Survey)

The Willis Towers Watson annual survey provides a wealth of information on global pensions and their asset allocations. Pension asset allocations around the world continue to show a move away from the simple equity and bond betas. The current survey shows only 75% of allocations are between equities, bonds, and cash with equities only given an allocation of less than 50%. These allocation numbers, however, show an increasing exposure to global equities and bonds. The other basket, representing the remaining 25%, includes real state and alternatives which can include a wide range of investment products. Pensions continue to move out of equity and bonds for alpha capital appreciation and income. The US equity allocation is down 10% since 2007 (60% to 50%) while the other category is up 10% from 18% to 28% over the same period.

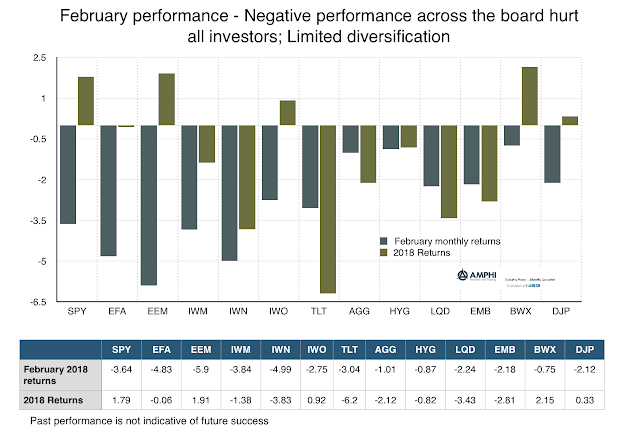

A Financial Shock And Change In The Market Environment – Not Good For Any Investor

There is little protection for investors when there is a price revaluation from a volatility shock. All equities styles declined in February. All equity sectors generated negative returns. Country equity returns were negative and bonds offered no protection. Correlations all moved higher in February although there are some interesting limited opportunities. A comparison of momentum from the prior month and three-month period show the strength of the reversals. Prices fell below short, medium and long-term trends except for few outliers.

Trends In Markets – Mixed Signals Suggest A Period Of Transition

A review of the trends that current exist across market sectors suggest that there is significant noise about directions and fundamental changes from last month. The equity bounce post the volatility shock seems to have played out and now new information such as “trade wars” seems to be defining new trends. Bonds seem to be moving back to the core negative correlation with equities. The dollar sell-off also seems to have paused except for traditional safe asset currencies. Metals are now trending down but commodities are responding to a weather shock. While there may be profitable opportunities later this month, current signals are mixed.

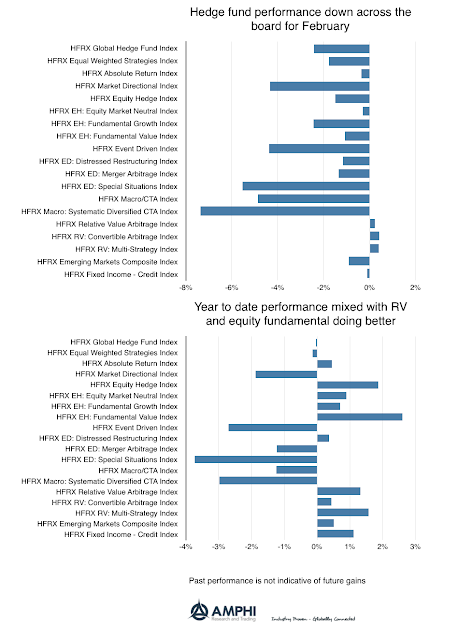

Hedge Fund Performance Sank With Equity Beta Decline

Hedge funds as measured by the HFR indices suffered with the overall market decline with only RV strategies being able to take advantage of the higher volatility environment. In general, the equity hedge fund declines were consistent with their longer-term betas (approximately .3 to .6). The outliers for the month were the event driven, special situations, macro and systematic CTAs indices. The year-to-date returns show significant dispersion with equity hedge fund indices generally positive while special situations, systematic CTAs, and event driven indices falling between -2.50 and -3.75 percent.

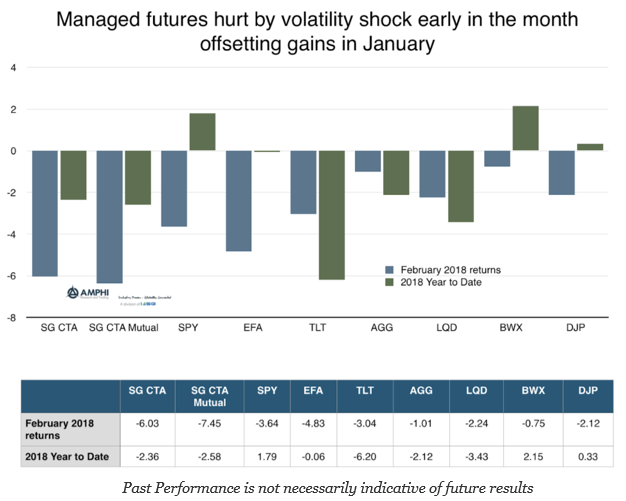

Managed Futures Managers Hurt By Volatility Shock

The managed futures hedge fund category generated poor performance in February as measured by the SocGen CTA index and the SocGen CTA mutual fund index. This behavior was also seen in the BTOP 50 index which declined 5.29 percent for the month. The SocGen short-term traders index was down 4.31 for the month but still up for the year by just over 1%. Nevertheless, the year to date return numbers for managed futures are better than long duration bond performance and the credit sector as measured by the TLT and LQD ETFs.

February Performance – Ouch! So Let’s Put In Context

February was a bad month for investment performance. All of the major ETF indices we normally follow were negative. Diversification was an elusive concept and reinforced the key portfolio allocation risks of rising correlation. There is no positive spin with these numbers other than less risky assets like bonds fell less than more risky assets, although year to date numbers show that bonds have not been a safe haven. There are a few takeaways from the month:

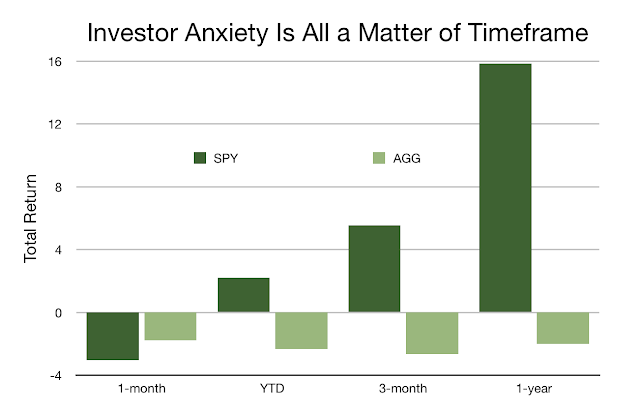

Investor Anxiety Is All a Matter of Timeframe

How would you feel about your investment portfolio if you went to sleep at the beginning of the year and woke-up on Friday? What if you stuck your portfolio in a drawer and pulled it out after three months or a year to look at performance? My guess you would say you were happy and comfortable with your investment decisions, yet there has been a lot of investor anxiety this month.

Financial Shocks Can Be Either Endogenous Or Exogenous – What Can We Expect?

There was a clear financial shock to the market with the spike in the VIX index earlier this month, but the market has reversed a significant portion of the earlier losses. From the SPY high in January, the market declined about 10.5%. There has been a reversal of 6% so the stock market is now positive for the year and only down 4.5% from the high and down 2% from month-end.

The “3 by 5 Index Card” on What You Need to Know About the February VIX Spike

University of Chicago professor Harold Pollack in an interview a few years ago mentioned that the best money advice can fit on a three-by-five inch index card. He was then challenged to write the card. His financial advice went viral. We follow this tradition by focusing on a simple “three-by-five index card” on the VIX volatility spike earlier the month.