Archives

Understanding Investor Preferences Is Not Easy – Just Ask Them

The line between recent “exotic preferences” and “behavioral finance” is so blurred that it describes academic politics better than anything substantive. – John Cochrane University of Chicago

John Cochrane, as well as others in finance, has focused on the academic issue of defining preferences for investors at an abstract level, but the issue becomes a reality when trying to extract preferences from investors to help build a portfolios.

Time Series or Cross Sectional Momentum – Which is Better? Your Choice May Matter

The marketplace is abuzz with the value of momentum trading, but a closer inspection shows that it is packaged in two major strains, time series and cross-sectional momentum. The traditional trend-following CTA focuses on time series momentum while the most of the equity research and implementation is conducted through the cross-sectional approach. There is similarity between these approaches, but there are also enough differences so that the return profile for each will not be the same.

If You Take Away the Fed Balance Sheet, Should the Bond Premium Be Negative? Term Premium Reality

The Wall Street talk is that all markets are over-valued, yet any valuation has to be placed in context. For fixed income, this is not easy given you have to make a judgment on both the real rate of return and expected inflation. Additionally, there is a need to measure the term premium associated with bonds. The premium measures the compensation necessary for investors to hold longer duration bonds versus a series of successive short bonds given the volatility and uncertainty associated with real rates and inflation. The term premium is not directly observable and is difficult to measure but has intuitive appeal.

Renaissance in Global Macro – It Is All About Global Disruption and “Creative Destruction” – Here Is One Avenue for Dislocation

Barron’s published a provocative piece from my friend John Curran, The Coming Renaissance of Macro Investing: The petrodollar system is being undermined by exponential growth in technology and shifting geopolitics. Coming: a paradigm shift. The concept behind this regime shift or dislocation ties together finance, technology, and global trade. Changes in the flow of trade based on shifting patterns of economic growth with disruptions in technology are going to spill-over to financial markets and prices. Capital flows are reactive to broader movements in power, politics, economic growth, and trade.

Zhou Xiaochuan – The Central Banker Even Quants Should Have Known. But Who Will Come Next?

You have heard of Yellen (Fed), Draghi (ECB), Kuroda (BoJ), and Carney (BOE), but most cannot name any China central banker, yet the moves of this bank may be more important than the four when thinking about the future of world currency hegemony. Zhou Xiaochuan has been in the news just before the Chinese Congress with a strong appeal for financial reform. This is reform for further ascent of China as a major financial player. He has followed this path across his central banking career, but he is set to retire in January.

Diversification Beyond 60/40: A Path to Improved Portfolio Performance

“Enough with this diversification talk, I’ve got my 60/40 and I am happy!” The 60/40 stock/bond portfolio mix has become a standard reference or benchmark for many investors, yet its performance versus a truly diversified portfolio is mixed.

Richard Thaler – Nobel Prize Winner – The Economist Who Provides a Foundation for Rules-Based Managed Futures

We congratulate Richard Thaler on winning this year’s Nobel Prize in Economics. His relentless research on the failings of rational behavior in human decision-making has had a significant impact in finance and economics. His prolific work is the foundation for all of what we call behavioral economic and finance. Prior to Thaler, economist focused on Homo Economicus, the rational man that does not make mistakes or misjudgments. Thaler showed through test after test that we make mistakes and have biases. He did this albeit radical work not as an outsider to finance like Dan Kahneman but as a economist steeped in the neoclassical tradition.

Back to Basics on Managed Futures with AIMA – Answering the Question for Why This Strategy Should be Held

There are many works on managed futures that explain the basics of this hedge fund strategy, but the characteristics need to be reinforced especially at current times when the strategy is underperforming other hedge fund strategies. The core reason for holding managed futures is that it provides useful diversification. This diversification is not available from other strategies and this diversification will be especially present during ‘bad times” of a equity decline. Don’t forget that those strategies that have more systematic risk will need to generate higher returns. Investors will be paid to hold them. On the flip-side, there will be a “payment” for managed futures which does well in “bad times”.

Is there a difference between smart and intelligent with hedge fund management?

An investor can ask, “Find me the most intelligent hedge fund manager. Someone else may say, “I want the smartest manager in the hedge fund space”. Saying that you want an intelligent manager may not be the same as saying you want a smart manager. There is a difference between intelligence and smarts, so says, Heather Butler in the recent Scientific American article, “Why do smart do dumb things, Intelligence is not the same as critical thinking and the difference matters”.

Return Rotation to Higher Risk Premium Equities Relative to Bonds

September was a month of transition for many styles, sectors, and class returns. In the style sector, small cap, growth, and value benchmarks generated strong performance under higher expectations for the reflation trade. There was a rotation from safer fixed income to higher risk premium styles. We are a long way from tax reform or a cut, but the fiscal issue is back on the table and in the minds of investors who want to get ahead of any changes.

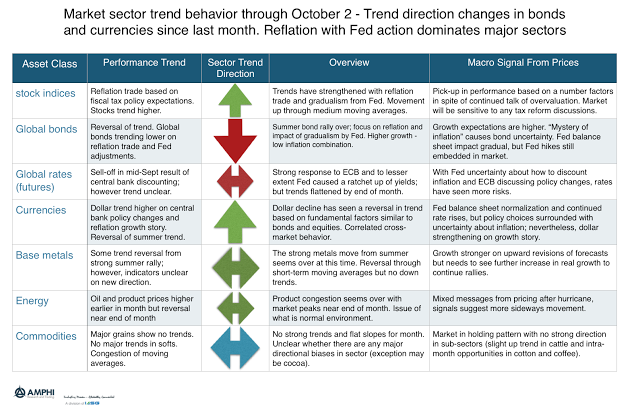

Change in Sector Trend Direction – Problems of September May Be Opportunity for October

The trend story for September was an end to the summer bond rally, a pick-up in equity trends, and a new interest in buying dollars. Without major strong trend opportunities in commodities, the reversal in bonds and currencies hurt many managed futures traders.

Bond Quality Down Further – Reason to Switch to Global Macro

Corporate spreads are tight and there is little room for further reduction given the absolute level of spreads. The reach for yield may be at an extreme. The bond spread is the compensation given bondholders for taking on the risk of corporate debt; consequently, it should become a concern when the quality of bond covenants or protections declines with spreads. Of course, if risk is declining, this is not the case, but at this point in the credit cycle it is hard to make that argument. An inverse relationship between spreads and covenant weakness means you are getting less compensation and less protection for the same risk, all things equal.

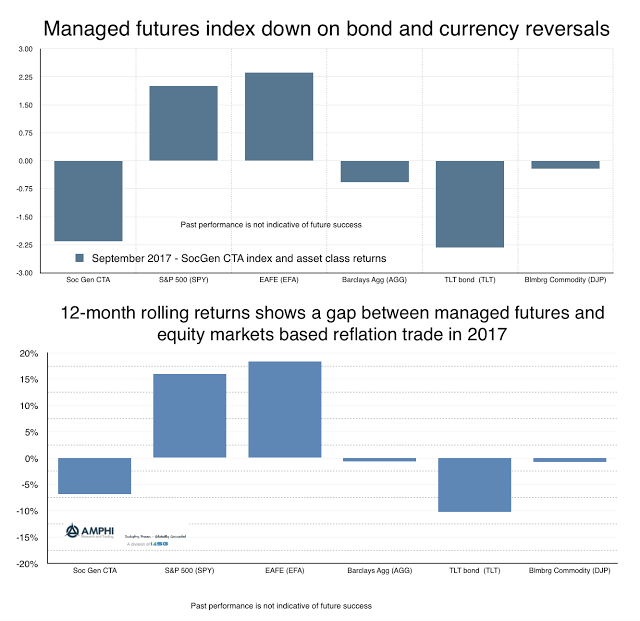

Managed Futures Turn Negative on the Renewed Interest in the “Reflation Trade”

Managed futures returns across CTA’s were down on average for September based on reversals in currency and bond trends. The weakening dollar and the strong bond returns during the summer made for good performance in July and August, but the combination of renewed interest in the Trump reflation trade and uncertainty concerning the direction of interest rates changed the trend opportunities.