Archives

Language, Perception, and Numbers – The Translation Problem

“March Hare: …Then you should say what you mean.

Alice: I do; at least – at least I mean what I say — that’s the same thing, you know.

Hatter: Not the same thing a bit! Why, you might just as well say that, ‘I see what I eat’ is the same as ‘I eat what I see’!

March Hare: You might just as well say, that “I like what I get” is the same thing as “I get what I like”!

The Dormouse: You might just as well say, that “I breathe when I sleep” is the same thing as “I sleep when I breathe”! – Lewis Carroll’s “Alice In Wonderland”

“If you cannot say what you mean, your majesty, you will never mean what you say and a gentleman should always mean what he says.” – Reginald Fleming Johnston (The Last Emperor)

“let your yea be yea; and your nay, nay.” – Matthew 5:37

I meant what I said and I said what I meant. An elephant’s faithful one-hundred percent. – Dr. Seuss book “Horton Hears a Who”.

When managers or investors use language, there can be a significant amount of uncertainty in what meant. There is little precision in language so quantitative analysis provides more details in the highly competitive money management field.

Momentum as the Big Embarrassment to Market Efficiency

“Momentum is a big embarrassment for market efficiency,” he proclaimed, saying he “hopes it goes away” and that the concept was “not exploitable.” – Eugene Fama from CFA Society of Chicago keynote speech. “Never let the truth get in the way of a good story.”― Mark Twain. You cannot help but think about Thomas Kuhn […]

Should I Care if a Managed Futures Fund has a Five-Star Rating?

So you see a manager with a good Morningstar rating. It has five-stars. Should an investor care? Past performance is not indicative of future returns, so should it matter if you had highly rated past risk-adjusted performance?

Certainly, a rating is not definitive, but as a heuristic on a fund’s relative performance, there is positive information to be gleaned from ratings.

A Difference between Theory and Practice

There is difference between theory and practice. The academic research study that identifies an obvious new risk premium may be difficult or impossible to implement in practice. The good firm is able to separate theory and practice and avoid implementing bad ideas. They will have a feel for whether it can be done in practice.

Networks and Plumbing – The Mechanics of Systemic Risk

Behind the backdrop of the vast changes in monetary policy over the post Financial Crisis period has been the movement to improve the regulatory environment for financial markets in order to reduce systemic risk. Significant work has been done to improve monitoring and rules to eliminate excessive speculative behavior, but as more regulations are proposed and more changes to the financial system are made, there is demising marginal benefit and a greater likelihood for unintended consequences. A rule that makes sense for one group may lead to a shift in risk capital and changes in behavior toward unregulated areas. Simply put, risky behavior will shift to the places where the cost of speculative behavior is least.

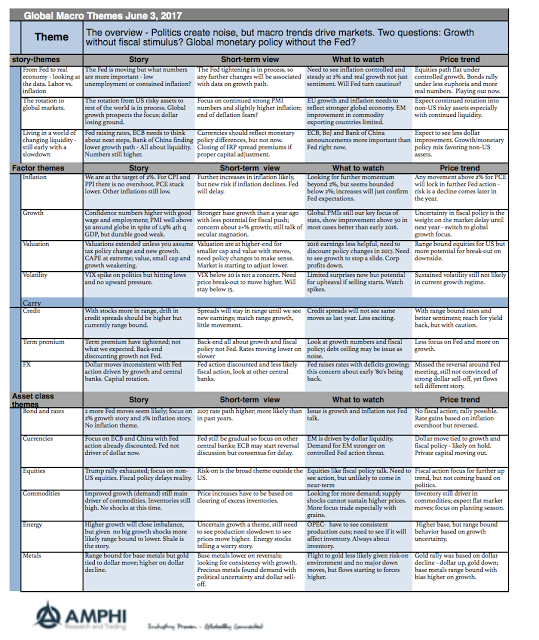

Global Macro in One Page – Forget the Noise and Watch the Numbers

As a more quantitative focused analyst, I keep focus one thing – the numbers. Stories are good, but numbers are better. At best stories, provide context for numbers, but stories of politics will not lead to market trends. Capital flows on trends in profits, growth, liquidity, and risk. Do not suffer from “shiny object” syndrome. The news of today may not impact the important fundamental trends.

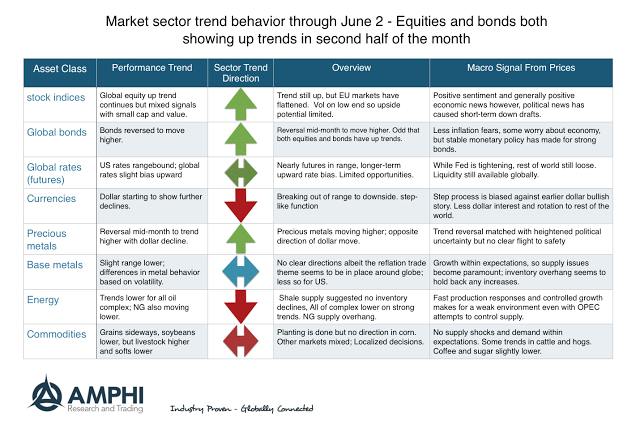

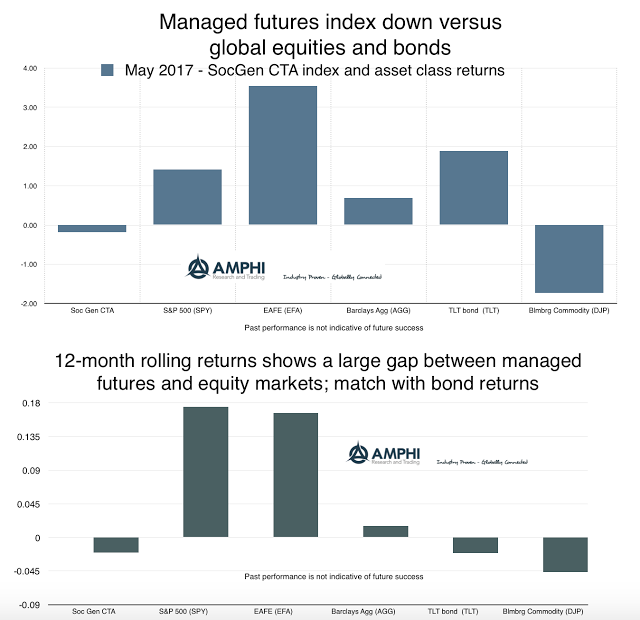

Sector Behavior Consistent with Economic Story but Wider Dispersion

While large cap and international stocks continued to move higher, the markets are starting to see more dispersion with small cap, growth, and value indices all posting negative returns for the month. The Russell value index has fallen to negative returns for the year. A growing dispersion is also evident in sector and country returns. Bonds have been a safe asset with positive gains for the year across all sectors. The returns are consistent with slow but positive growth around the world with controlled inflation.

Trends for June – Up for Equities and Bonds

May was a mixed month for many trend-followers. Some did well while others got caught on the wrong side of mid-month reversals. The month saw a mid-month equity sell-off which could have stopped-out a number of key positions in equities and bonds. This sell-off was based on political uncertainty and not macro fundamentals.

Managed Futures – All dressed up but not Going Anywhere

Money has flowed into managed futures under anticipation that there will be a crisis event that will need the diversification benefits of trend-following strategies. These investors adjusted portfolios away from perceived overvalued assets to the value from long-short diversified trend-following. What is the sense of increasing allocations after the divergent event of a equity sell-off?

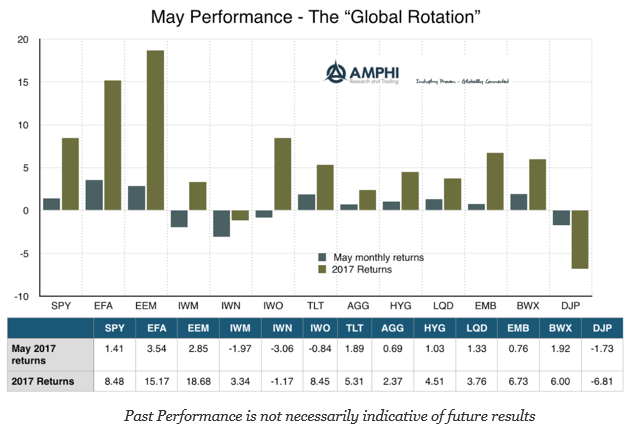

Asset Class Performance – The “Global Rotation”

Call it the “Global Rotation”, but last month was a continuation of what we have seen for the year. There has been a flow of money into international stocks and increasing divergence between the rest of the globe and US risky assets. There is a dollar adjustment component to these returns, but there is no mistake that there is a preference for cheaper opportunities around the world.

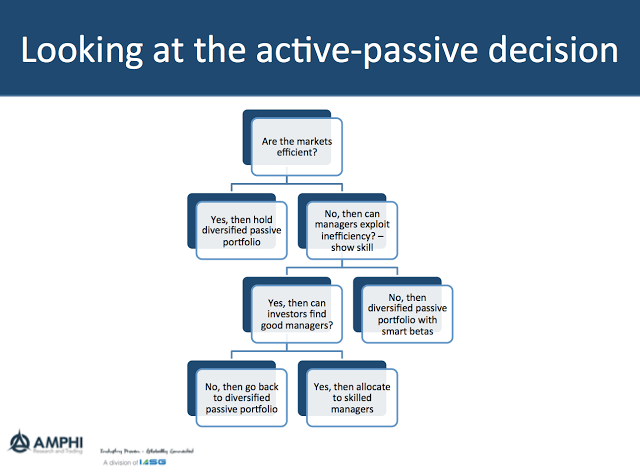

Simplifying the Choice Between Active and Passive Investing

The choice between active and passive investing has been a battle that has been raging for years, but it can be simplified through a set of easy questions. The answers to these questions are not easy, but by forming a direct set of straightforward questions with a decision tree, the issues can be discussed in […]

Avoid Atheoretical Data Analysis – A Rule for any Data Specialist

The process of scientific discovery, even within finance, is essential. One approach to finding new strategies could be to generate observations and then provide explanations, such as an inductive approach. The other is to first form a theory and then test a hypothesis, deductive reasoning. Much of machine and statistical learning is inductive reasoning, where […]

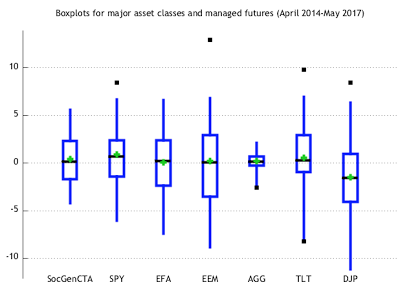

Looking at Asset Class Risk through Boxplots

Investors are so used to looking at standard deviation to define risk that they forget some easy exploratory data analysis tools that can be very helpful. The boxplot focuses on a greater description of the data through a simple display of a brand array of information. The box is formed by the first and third quartiles, the whiskers are 1.5 times the interquartile range, the green diamond is the average, and the black boxes are the outliers.