Archives

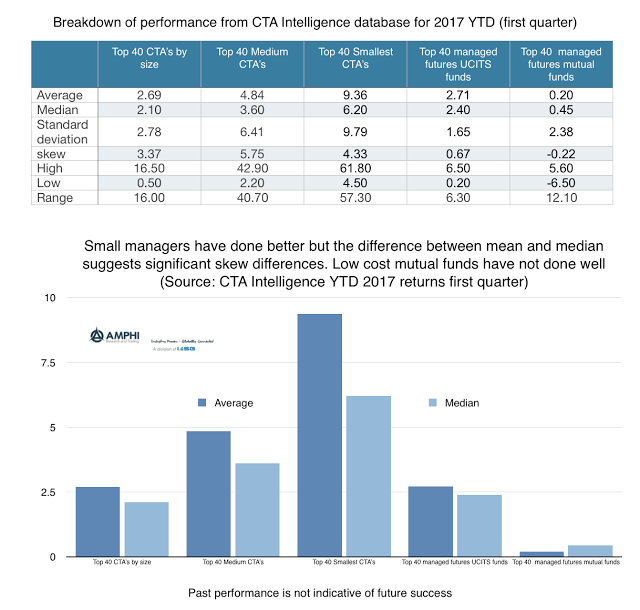

Size Matters with Managed Futures but Not Just with Performance

There has been a preference for large managers within the managed futures space as measured by money flows, but it comes at a cost. Looking at year to date performance from the CTA Intelligence performance database shows the differences in performance based on size. What is clear is that the average performance of a set of 40 small managers is significantly higher than the performance of the largest 40 managers. Going down in size will allow clear increases in average return and with median returns; however, a closer look shows that the price of obtaining higher returns can be high in terms of regret.

Trading Gold Futures – CME vs. LME – This Could be an Interesting Battle

With a new regulatory environment, the traditional gold market is up for grabs. While many of the changes have not been direct to the gold market but based on a broader environment, regulation is changing the market structure for trading in gold. Regulations which increase the cost of trading over-the-counter has and will push gold trading onto exchanges, centralized counterparts (CCP’s). This environmental change is the opportunity for new exchange entrants in the gold market. We have already seen new trading through ETF’s over the last few years change gold dynamics and now there is the opportunity for changes in futures trading.

The Effectiveness of Managed Futures: Exploring Trend-Following Strategies

Why is managed futures or, more precisely, trend-following an effective investment strategy? Many managed futures programs have been successful by keeping it simple and using heuristics like following the price trend and not always using all the available information about a market. Disciplined and systematic decision-making seems to be a robust means of dealing with […]

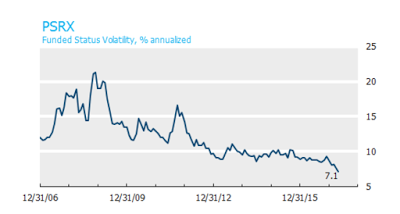

Pension Surplus Risk at all Time Lows

The Funded Status Volatility index (PSRX) from NISA is a useful tool for understanding pension risk exposures. It is an aggregate of the risks for pension based on the combination of assets and liabilities associated average allocations for the 100 largest pension funds as measured through public information and 10-k filings. The index, which represents $1 trillion in AUM, will move up and down with the volatility of all asset classes. Hence, falling equity and bond volatility as well as changes in the discount rates will translate into a falling PSRX index.

Volatility and Managed Futures – Is There a Relationship with the VIX?

Many believe that managed futures is a long volatility strategy because the strategy is like being long a look-back straddle. We believe there is a more nuanced story associated with long gamma exposure, but let’s use the prevailing wisdom of long volatility as a starting point for a discussion.

How Many Managers Should You Review Before You Pick One?

Choices, choices, choices. There are just so many managers to choose for a portfolio. Look at the major database; hundreds of managers of all sizes, styles, and skills. Using some simple criteria, the list can be reduced significantly. Minimum size, minimum track record, max drawdown, and max volatility could be just a few ways of […]

Quant Research and Managed Futures – Key Areas of Focus

Managed futures research is hard. This is especially the case in the quantitative area. There always are new models being tested by almost all managers, but finding a truly new model or process that adds value is truly difficult. Data mining is an issue.

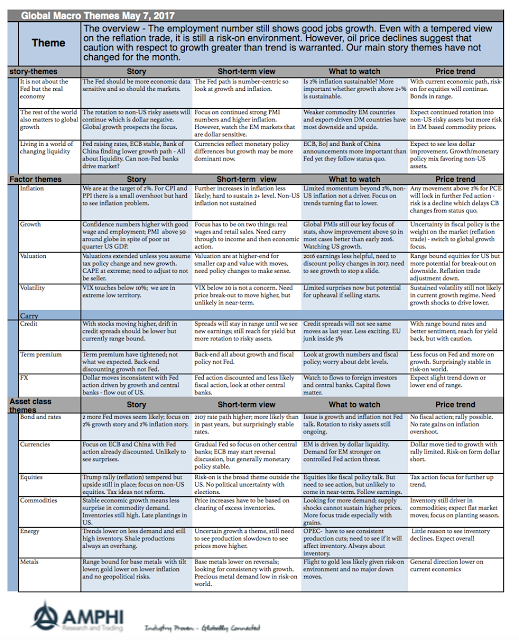

Global Macro on One Page – May 2017

The Fed and other central banks are not that important in the current thinking of investors. The focus is not on the policy musings of bankers but the real economic data. All that matters is whether growth has a strong chance to be above trend and whether global DM inflation has a chance of reaching and sustaining 2%. We are skeptics of both occurring.

The Importance of Liquidity in Metals Exchange and Futures Contracts

There should not be a lengthy discussion on what investors want from a metals exchange or futures contract—liquidity, liquidity, and liquidity. We use the word three times for each liquidity form that attracts trading. It does not matter if you are a hedger or speculator; the demand is the same; deep liquidity, so the cost […]

VIX and What to Expect – The Odds Against the Big Jump

The VIX index, the most widely watched measure of market volatility, is at extended lows with a jump lower after the French presidential first round election results. The uncertainty and risk premium from this election has been taken out of the market. Economic uncertainty has also fallen since the US election although it is still elevated since the earlier last fall.

Commodity Investing – What is it all About?

What is commodity investing all about: 1. The curves and carry – backwardation/contango (inventory). Given the cash market for commodities is often not available for investing, the primary market for investors in commodities is the futures. Consequently, the shape and dynamics of the futures curve is a dominant factor for longer-term investing. Investors cannot think […]

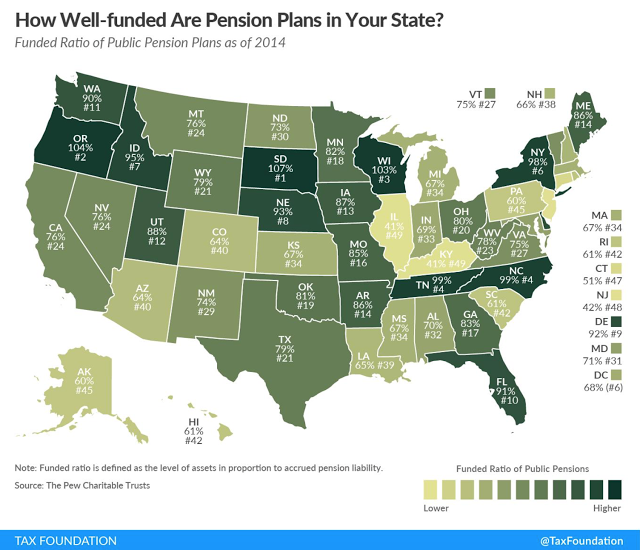

Who Needs Alternatives Like Managed Futures the Most? Underfunded State Pensions

The Tax Foundation map of state funding ratios for public pensions is very sobering. The amount of state under-funding is significant. These numbers are determined by the discounted expected liabilities relative to the assets held. To stay even with these ratios and assuming there is no surprise increase in liabilities, the states have to return the discount rate. These discount rates or expected returns seem unrealistically high.

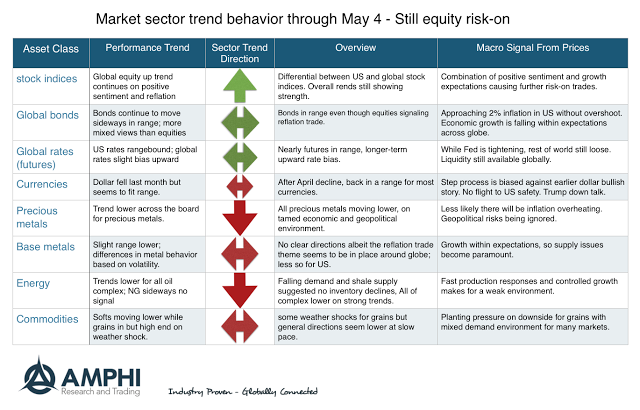

Market Trends for May – Some Developing Strength

Going into the month, there are good up trends in place with global equities and down trends in oil, precious metals, and selected commodities. What is interesting is the inconsistency across some markets sectors. The reflation risk-on trade is still apparent in the global equity indices, but we are not seeing strong evidence of bond sell-off or rally. Oil prices suggest both supply strength and demand weakness. Gold and precious metals are out of favor with long-only investors. The idea that we will have a dollar rally on Fed hikes seems misplaced and there is less risk-on demand for the US relative to the rest of the world.