Archives

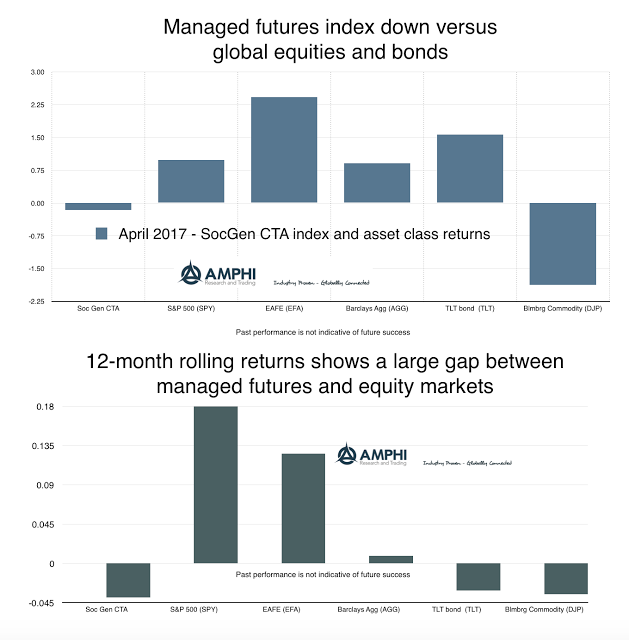

Managed Futures Flat for Month of April

The SocGen CTA index was essentially flat for the month which is not surprising given three major factors. One, we are in a global risk-on environment which generally is not attractive for trend-followers. It is not that there are no trends, but there were limited gains from diversification across asset classes relative to a risk-on portfolio. Two, there were few strong trends going into the beginning of the month. Given the usual time-frame for effective trend-following which is weeks not days, there has to be continuity of trends to have a good performance month. The strong gains in foreign markets may not have been given enough exposure to generate good portfolio returns. Three, the focus on financials especially fixed income and currencies by large managers was a drag on performance relative to equities and short commodities trends. Four, volatility is at extreme lows. We have looked at market volatility through the VIX index and current levels are above the 98th percentile for the lowest since 1990. Divergent strategies based on taking advantage of the spread in prices through time will be limited in their return potential in this type of environment.

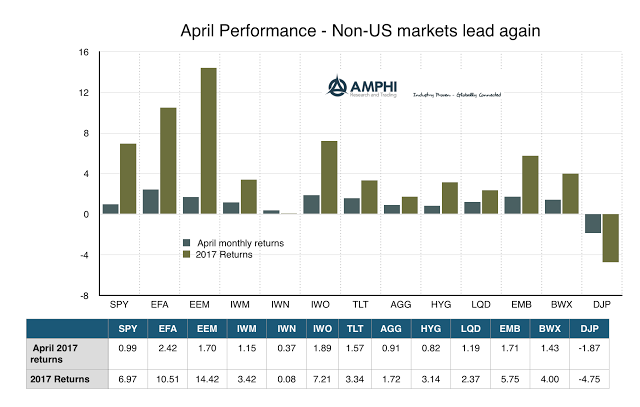

Sector Analysis Supports the Risk-On Market Sentiment

The positive equity performance for April and the strong year-to-date returns show that the risk-on environment continues. What is noticeable is the switch to global and emerging market gains although this has been helped by the declining dollar which may have added about one percent to performance. Performance has rotated from the reflation trade in the US to a broader investment in global equities.

Fat-Tails Everywhere Even if Volatility is Low

I was reviewing an interesting research piece from Covenant Capital on kurtosis across different assets traded in the futures markets. They offer a spreadsheet tool that can allow anyone to find the number of fat-tailed occurrences relative to a normal distribution. The data show that there are fat-tails everywhere across all asset classes. We do […]

Strong Gains around the Globe for Risky Assets

It is a risk-on world with global equities (EFA) and emerging markets (EEM) now posting double digit gains for the year. A first round French election that was pointed less in the direction of Le Pen and a Trump presidency that does not seem as extreme as some pundits suggested has been coupled with global economic growth that is stronger than expected. The deflation trade may be further tempered in the US, but the threat of trade wars has diminished and the world economy is more focused on reality than dire economic scenarios.

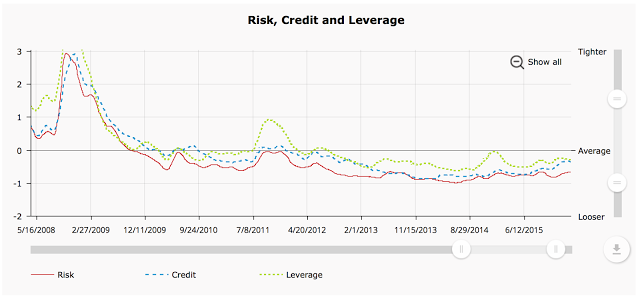

Always Check the Financial Conditions – Still Loose

There are many narratives for why equities or bonds will move higher, but a recurring theme is the financial conditions faced by investors. Financial conditions provide the tailwinds or headwinds to push asset class returns. These conditions tell us something about whether we will be transitioning between a risk-on and risk-off environment or whether we will be a crisis mode.

The Real Bias – Stock Optimists versus Bond Pessimists

During a simple discussion on investing, the topic turned to biases. We have learned to talk about many biases from behavioral economics. We now have a catalog of preferences which makes them easier to mitigate. Still, there seems to be one bias that is very hard to address, and that is the overarching theme of […]

Determine What Goes Wrong with Your Investment Model

How do you know whether a model is broken? Or, how do you conduct a model review? There are many specific steps for any review but there are four major questions that have to be addressed that are separate from risk management. The key question of model efficacy should focus on forecasting skill and action. Does the model forecast correctly and is the model employed properly to make good decisions.

Preparing for Market Risk – Stay Diversified Across Asset Classes, Factors, and Strategies

You get recessions, you have stock market declines. If you don’t understand that’s going to happen, then you’re not ready – you won’t do well in the markets. If you go to Minnesota in January, you should know that it’s gonna be cold. You don’t panic when the thermometer falls below zero.

-Peter Lynch

Follow the World Business Cycle – Economies are Integrated

Globalization is a critical part of macro investing. There can be talk of separation politics, but for investors, you have to focus on the global economic cycle because the world is highly integrated. What is very interesting is that globalization has been fairly stable between the current environment and the Bretton Woods period as discussed by the recent work of Eric Monnet and Damien Puy who studied long horizon data available from the IMF. They find that there were two common shock periods which caused a highly synchronous global behavior. The first was oil shock period of the 70’s and the second was the Great Financial Crisis. You could say that these were the two periods when “correlations went to one” across asset classes. There was no international diversification benefit.

“Winner‐Take‐All” Dynamics and Hedge Fund Investing

A growing stream of thinking in microeconomics is the concept of “winner-take-all” dynamics. The idea seems simple. A combination of networking economics and classic economies of scale creates situations where there are just a few dominant firms or economic agents who are able to capture significant market share in a given industry. With the advances in technology over the last decade, many industries are seeing the impact of winner-take-all dynamics leading to the result of greater concentration.

Populism and the Market: Assessing Risks for Investors

There has been tremendous talk concerning populism and politics, but for investors, the focus still must be on these movements’ economic and market impact. So discount the news headline and rhetoric and focus on the potential market impact, but a good definition of populism is necessary for building a framework to determine risks. Defining Populism […]

The Role of Factors in Finance: A Focus on Global Macro Investing

What has been at the vanguard of thinking in finance is the breakdown of returns into their constituent parts or risk factors. Finance has moved well beyond market beta. The first breakdown for a portfolio is not returns by asset class but returns by risk factors. Some have criticized the current situation as a factor […]

Why a Buy-and-Hold Strategy in Commodity Index Investing May Not Work

An article in the Wall Street Journal, “Why Commodity-Index Investing May be Futile,” has attracted much interest from investors. However, there was no new information in the story. The reasons for avoiding commodity indices should be taken seriously; nevertheless, the broader issue of differences between commodity and equity investing is straightforward. Commodity investing in an […]