As we better understand the return generation process, we are able to dissect any set of money manager or hedge fund returns into its component parts. At a high level, any money manager can be divided into a set of risk factors or premia and alpha or skill. As a general conclusion, researchers have found that as investors get better at identifying risk factors, the size of alpha declines. We are able to attribute more returns to specific risks so the amount that is leftover as skill declines.

Additionally, as we find that hedge funds returns are associated with specific identifiable and repeatable risk premia, there is a greater desire to change the fee model based on the risks taken. If the majority of hedge fund returns are associated with compensation for specific risks taken, the idea of paying incentive fees seems odd. The incentive fee eats into the return compensation for risk. The incentive fees should be paid on alpha or the uniqueness of return generation and not on the risk exposures.

Investors should pay for and celebrate alpha skill, but pay a different price for specific risk exposures. We are not arguing that money management for specific risk premia should be free, nor should the dynamic management of risk premia be dismissed as easy work, but there should be a better awareness of the different types of work associated with fund generation.

There is now a wide-range of alternative risk premia (ARP) that can be obtained at relatively low cost through the swaps market. A close look at some of these risk premia portfolios suggests that they provide similar and in many cases better returns than what can be received from hedge funds. These risk premia can be structured as a rules-based investing at a price that should be lower than the normal fee schedule.

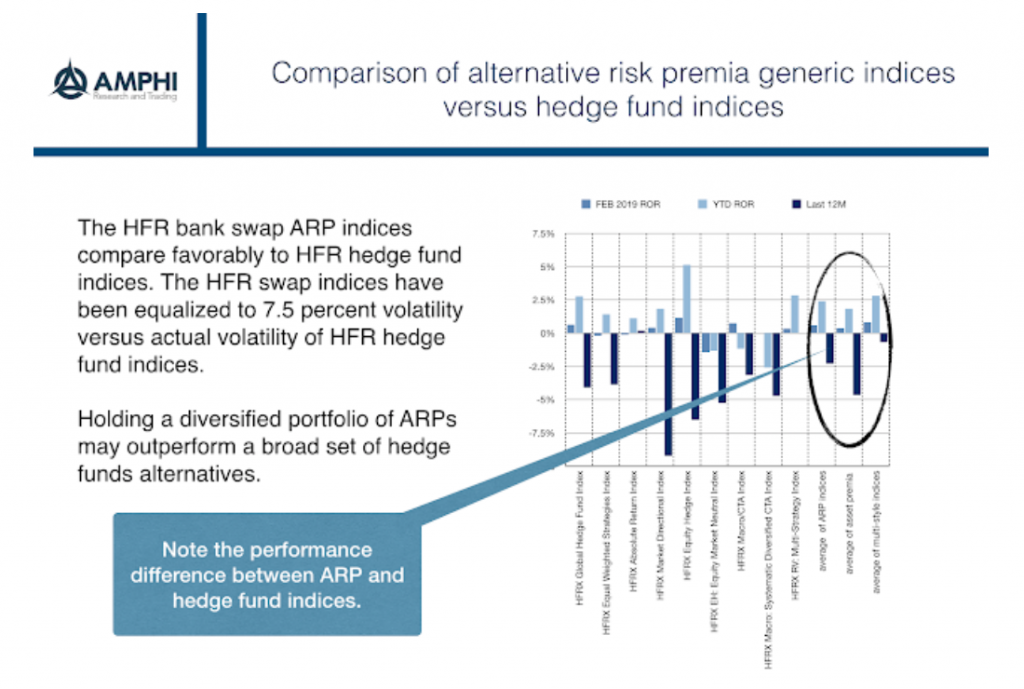

We compared the average return of ARP indices across asset classes and multi-strategies for asset class as well as an average of these two HFR ARP categories against some broad-based HFR hedge fund index categories. While not an extensive time series analysis, the recent returns show that ARP average returns are comparable and, in many cases, better than average hedge fund returns. The mapping between the hedge fund indices and ARPs has not been done through regression, but the general concept shows that bundled risk premia can give the same return profiles as hedge funds.

ARPs can be used as a core strategy for liquid alternative investing and hedge funds with specialized skills, or unique strategies that cannot be easily replicated through rules can serve as satellites. Invest in the best hedge funds, but if they cannot be found, use alternative risk premia delivered through total return index swaps.